Stock Spotlight: CAR Group Limited (ASX:CAR)

About CAR Group Limited.

CAR Group Limited engages in the online vehicle marketplace business in Australia, New Zealand, Brazil, South Korea, Malaysia, Indonesia, Thailand, Chile, China, and North America. The company operates through six segments: Australia " Online Advertising Services; Australia " Data, Research and Services; Investments; North America; Latin America; and Asia segments. It offers classified advertising that allows private and dealer customers to advertise automotive and non-automotive goods and services for sale across the carsales network; products, including subscriptions, lead fees, listing fees, and priority placement services; and display advertising services, such as placing advertisements for corporate customers comprising automotive manufacturers and finance companies. The company also provides software as a service, research and reporting, valuation, appraisals, and website development and hosting services, as well as photography services. In addition, it offers vehicle inspection services; operates digital automotive and non-automotive marketplaces; and offers automotive data and advertising services. The company was formerly known as carsales.com Ltd and changed its name to CAR Group Limited in November 2023. CAR Group Limited was incorporated in 1996 and is headquartered in Melbourne, Australia.

Source: EODHD

Key Stats

Key Stats

Source: EODHD. Data as of 17/02/26.

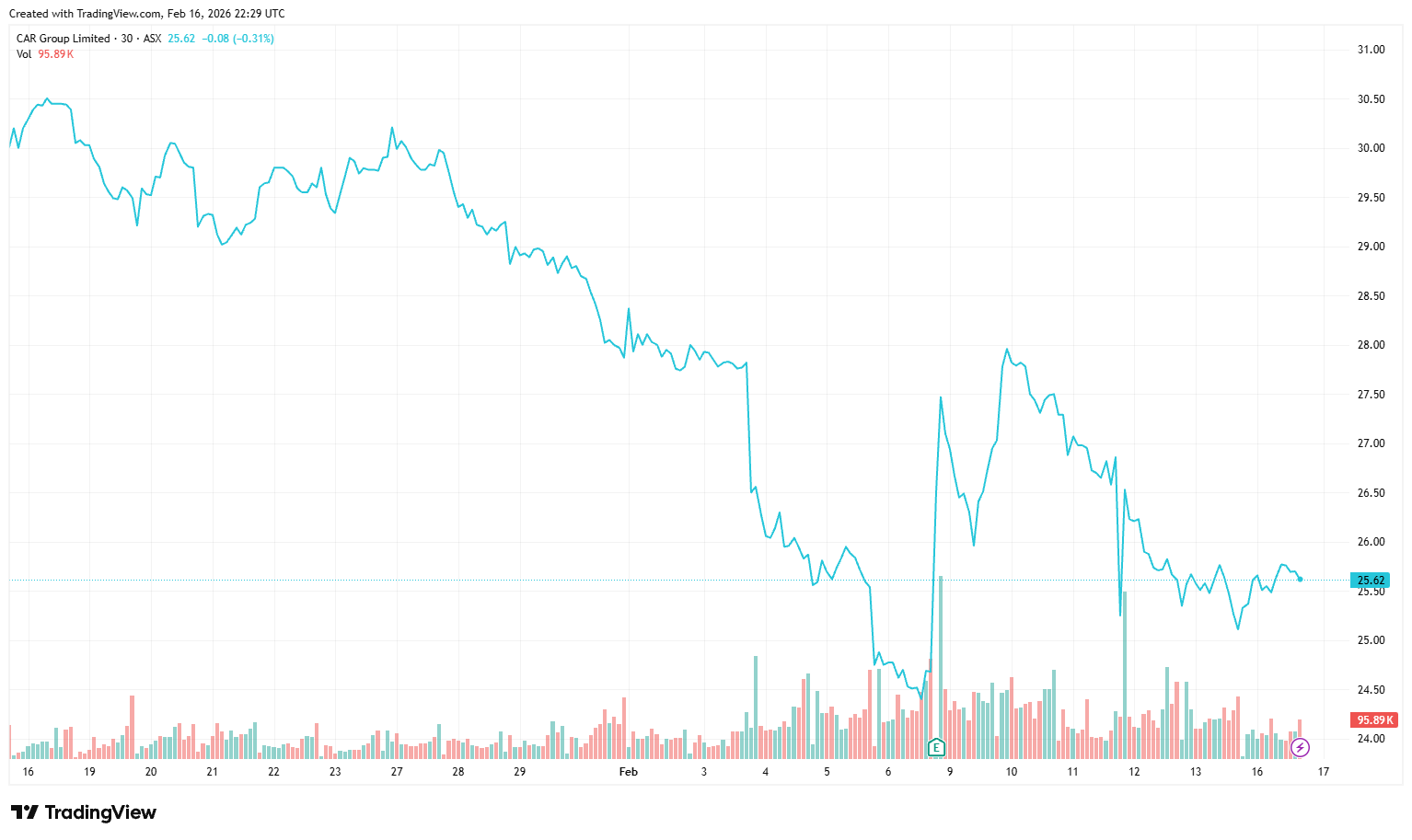

Price Performance

Growth Potential

- Recent share price derating has improved the overall attractiveness of CAR’s valuation, trades well below our revised price target and is not offering solid dividend yield for income focused investors.

- Leading market position in online car classifieds in Australia.

- Overseas expansion provides new and higher growth opportunities – e.g. South Korea, North America, and Brazil.

- Increasingly diversified geographic coverage into underpenetrated markets.

- Bolt-on acquisitions provide opportunities to supplement organic growth.

- The Company can sustain high single-digit to low double-digit revenue growth. We also forecast double digit earnings growth over the next 3 years.

- CAR’s move into adjacent products and industries.

- Looking to take more of the car buying experience online with dealers (i.e. increasing its total addressable market).

- Product innovation helps drive increased moat around CAR’s market position (e.g. recent launch of C2C Payments)

Key Risks

- Trading on elevated trading multiples.

- Unable to push through price increases to end customers.

- Competitive pressures - that is car dealer driven substitute platform or the No. 2 & 3 player gain ground on CAR.

- Subdued motor vehicle sales – especially used vehicles market.

- Value destructive acquisition / execution risk with international strategy.

- Not immune from broader downturn in economy (consumer likely to delay a significant purchase in time of uncertainty).

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

Speak to an Advisor