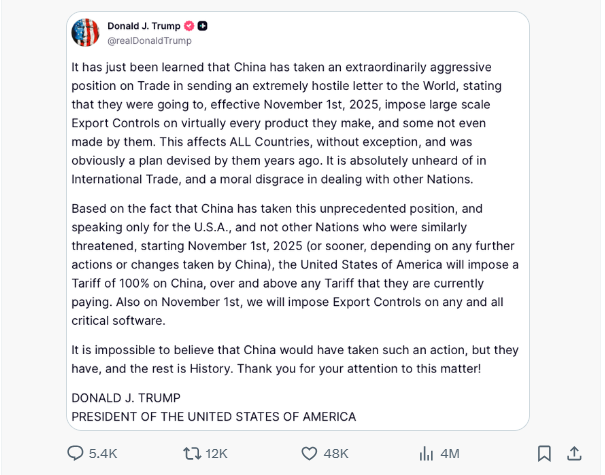

Trump’s Post Triggered a $2 Trillion Market Slide

The announcement triggered a sharp global equity sell-off. U.S. markets reacted immediately, with the S&P 500 falling 2.7% and the Nasdaq Composite dropping 3.6%, their steepest one-day declines since April 2025. The move underscored how sensitive markets remain to abrupt trade policy shifts, particularly those with wide-reaching global implications.

Market Reaction: From Rhetoric to Risk-Off

Investors interpreted Trump’s statement as more than campaign rhetoric, viewing it as a credible policy shift with near-term economic consequences. The timing and breadth of the proposed tariffs reignited fears of a renewed trade war, further eroding sentiment already weakened by slowing growth and persistent inflation concerns.

The market response was swift and broad-based. Global equities shed nearly USD 2 trillion in value as algorithmic systems and hedge funds accelerated selling. Technology, semiconductor, and industrial sectors bore the brunt of the downturn as investors priced in higher production costs, disrupted supply chains, and weaker profit margins. Companies heavily reliant on Chinese manufacturing or export markets were hit hardest.

In contrast, defensive sectors such as utilities and healthcare held up relatively well as investors sought stability. Safe-haven demand strengthened, pushing gold and the U.S. dollar higher, while Treasury yields declined as capital rotated into bonds. Market volatility surged, highlighting uncertainty over how aggressively either side might act in the coming weeks.

For many market participants, the sell-off was less about the tariff measure itself than what it represented: a shift back toward unpredictable trade confrontation. The potential for tit-for-tat retaliation raised renewed concerns over inflation, earnings downgrades, and slowing global growth.

Broader Economic & Policy Implications

The proposed tariffs pose several key risks for both markets and policymakers.

Inflation and cost pass-throughs:

Higher import duties are likely to lift input costs for manufacturers, filtering into consumer prices and complicating the Federal Reserve’s inflation management.

Margin pressure and earnings guidance:

Technology and manufacturing companies dependent on foreign components may face tighter margins and could be forced to revise earnings outlooks or delay capital expenditure.

Trade retaliation:

Beijing has already signalled potential countermeasures, increasing the risk of a broader trade escalation affecting multiple sectors and regions.

Growth effects:

Slowing trade activity, reduced investment confidence, and rising uncertainty could weigh on global GDP growth, particularly across export-driven economies.

China market impact:

Chinese equities also appear vulnerable, with investors expecting profit-taking and capital outflows amid heightened risk aversion.

What Investors Should Consider

Given heightened volatility and policy uncertainty, portfolio positioning requires greater selectivity. Investors may consider focusing on companies with solid balance sheets, resilient cash flows, and minimal exposure to cross-border trade disruptions.

Defensive sectors such as healthcare, consumer staples, and utilities could offer relative stability if global tensions persist. Maintaining liquidity and flexibility remains essential, enabling investors to respond swiftly to policy updates or market corrections.

For long-term investors, the sell-off may also present selective opportunities. Quality companies that have been oversold during the downturn could merit reassessment, provided their underlying fundamentals remain intact. Monitoring leading indicators such as Chinese trade data, tariff announcements, and corporate guidance will be critical to assessing the trajectory of market sentiment.

Outlook

The scale and speed of the recent sell-off demonstrate how geopolitical developments have become a central driver of equity valuations. Trade and policy communication now carry direct market implications, shaping expectations for inflation, earnings, and capital flows.

For investors, the coming weeks will hinge on whether tensions ease or intensify ahead of the 1 November deadline. Until greater clarity emerges, maintaining discipline, diversification, and downside protection will be essential to navigating a market environment increasingly defined by political risk.

If you would like to discuss how these developments could affect your portfolio, speak with one of our advisers.

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

Speak to an Advisor

As AI becomes cheaper to deploy, could the next investment winners shift beyond chipmakers? Explore how the AI cost race is redefining future tech leaders.

Get the latest on Santos Limited (ASX:STO), including stock performance, technical analysis, forecasts & key insights. See if STO supports your goals.

Big Tech earnings could shake your portfolio this week. Understand how the latest results may influence global markets, the ASX and your investment strategy.

A second strategic chokepoint is under threat after Hormuz. Discover how the Bab al-Mandeb blockade could affect oil prices, inflation, interest rates and your portfolio.

This week's Stock Spotlight is NYSE-listed JPMorgan Chase & Co. About JPMorgan Chase & Co. JPMorgan Chase & Co. operates as a bank and financial holding company in the United States, rest of North America, Europe, the Middle East, Africa, the Asia Pacific, Latin America, and the Caribbean. It operates in three segments: Consumer & Community Banking, Commercial & Investment Bank, and Asset & Wealth Management. The company offers deposit, investment and lending products, and cash management; mortgage origination and servicing activities; residential mortgages and home equity loans; and credit cards, payment solutions, travel services, merchant offers, lifestyle benefits, auto loans, and leases to consumers and small businesses through bank branches, ATMs, and digital and telephone banking. It also provides investment banking, market-making, financing, custody, and securities products and services; corporate strategy and structure advisory, equity and debt market capital-raising, and loan origination and syndication services; cash and derivative instruments, risk management solutions, prime brokerage, clearing, and research; and fund services, liquidity and trading services, and data solutions products for large corporations, financial institutions, merchants, start-ups, small and midsized companies, local governments, municipalities, nonprofits, and commercial real estate clients. In addition, the company offers multi-asset investment management solutions in equities, fixed income, alternatives, and money market funds to institutional clients and retail investors; retirement products and services, estate planning, lending, deposits, and investment management products to high-net-worth clients; and financial transaction processing. JPMorgan Chase & Co. was founded in 1799 and is headquartered in New York, New York. Source: EODHD Key Stats

This week's Stock Spotlight is NYSE-listed Wells Fargo & Company. About Wells Fargo & Company. Wells Fargo & Company, a financial services company, provides diversified banking, investment, mortgage, and consumer and commercial finance products and services in the United States and internationally. It operates through four segments: Consumer Banking and Lending; Commercial Banking; Corporate and Investment Banking; and Wealth and Investment Management. The company's financial products and services includes checking and savings accounts, and credit and debit cards, as well as home, auto, personal, and small business lending services. It also provides personalized wealth management, brokerage, financial planning, lending, private banking, trust and fiduciary products and services; and financial solutions to private, family owned and public companies through products and services including banking and credit products across multiple industry sectors and municipalities, secured lending and lease products, and treasury management. In addition, it offers a suite of capital markets, banking, and financial products and services, such as corporate banking, investment banking, treasury management, commercial real estate lending and servicing, equity, and fixed income solutions, as well as sales, trading, and research capabilities services to corporate, commercial real estate, government, and institutional clients. Wells Fargo & Company was founded in 1852 and is headquartered in San Francisco, California. Source: EODHD Key Stats

This week's Stock Spotlight is NYSE-listed Bank of America Corp. About Bank of America Corp. Bank of America Corporation, through its subsidiaries, provides various financial products and services for individual consumers, small and middle-market businesses, institutional investors, large corporations, and governments worldwide. It operates through four segments: Consumer Banking, Global Wealth & Investment Management (GWIM), Global Banking, and Global Markets. The Consumer Banking segment offers traditional and money market savings accounts, certificates of deposit and IRAs, checking accounts, and investment accounts and products; credit and debit cards; residential mortgages and home equity loans; and direct and indirect loans. The GWIM segment provides investment management, brokerage, banking, and trust and retirement products and services; wealth management solutions; and customized solutions, including specialty asset management services. The Global Banking segment offers lending products and services, including commercial loans, leases, commitment facilities, trade finance, and commercial real estate and asset-based lending; treasury solutions, and underwriting and advisory services. The Global Markets segment provides market-making, financing, securities clearing, settlement, and custody services; securities and derivative products; and risk management products using interest rate, equity, credit, currency and commodity derivatives, foreign exchange, fixed-income, and mortgage-related products. Bank of America Corporation was founded in 1784 and is based in Charlotte, North Carolina. Source: EODHD Key Stats

This week's Stock Spotlight is NYSE-listed Citigroup Inc. About Citigroup Inc. Citigroup Inc., a diversified financial service holding company, provides various financial products and services to consumers, corporations, governments, and institutions. It operates through five segments: Services, Markets, Banking, U.S. Personal Banking, and Wealth. The Services segment includes treasury and trade solutions, which provides cash management, trade, and working capital solutions to multinational corporations, financial institutions, and public sector organizations; and securities services, such as cross-border support for clients, local market expertise, post-trade technologies, data solutions, and various securities services solutions. The Markets segment offers sales and trading services for equities, foreign exchange, rates, spread products, and commodities to corporate, institutional, and public sector clients; and market-making services, including asset classes, risk management solutions, financing, and prime brokerage. The Banking segment includes investment banking services comprising equity and debt capital markets-related strategic financing solutions; advisory services related to mergers and acquisitions, divestitures, restructurings, and corporate defense activities; and corporate lending consists of corporate and commercial banking. The U.S. Personal Banking segment provides proprietary and co-branded card portfolios; and traditional banking services to retail and small business customers. The Wealth segment offers financial services to high-net-worth clients through banking, lending, mortgages, investment, custody, and trust product offerings; professional industries, including law firms, consulting groups, accounting, and asset management; and affluent and high net worth clients. The company operates in North America, the United Kingdom, Japan, North and South Asia, Australia, Europe, the Middle East, and Africa. Citigroup Inc. was founded in 1812 and is headquartered in New York, New York. Source: EODHD Key Stats

AI is driving unprecedented demand for data centres. Discover how the infrastructure powering AI is creating opportunities across energy, property and technology.

About Capstone Copper Corp. Capstone Copper Corp., a copper mining company, mines, explores for, and develops mineral properties in the United States, Chile, and Mexico. The company primarily explores copper, silver, gold, molybdenum, zinc, iron, cobalt, and other base metals. Capstone Copper Corp. is headquartered in Vancouver, Canada. Source: EODHD Key Stats