Stock Spotlight: Cheniere Energy Inc (NYSE:LNG)

About Cheniere Energy Inc

Cheniere Energy, Inc., an energy infrastructure company, primarily engages in the liquefied natural gas (LNG) related businesses in the United States. The company owns and operates the Sabine Pass LNG terminal in Cameron Parish, Louisiana; and the Corpus Christi LNG terminal near Corpus Christi, Texas. It also owns and operates the Creole Trail pipeline, a 94-mile natural gas supply pipeline that interconnects the Sabine Pass LNG Terminal with several interstate and intrastate pipelines; and the Corpus Christi pipeline, a 21-mile natural gas supply pipeline that interconnects the Corpus Christi LNG terminal with interstate and intrastate natural gas pipelines. In addition, the company engages in the LNG and natural gas marketing business. Cheniere Energy, Inc. was incorporated in 1983 and is headquartered in Houston, Texas.

Key Stats

Key Stats

Source: Yahoo Finance. Data as of 16/09/25.

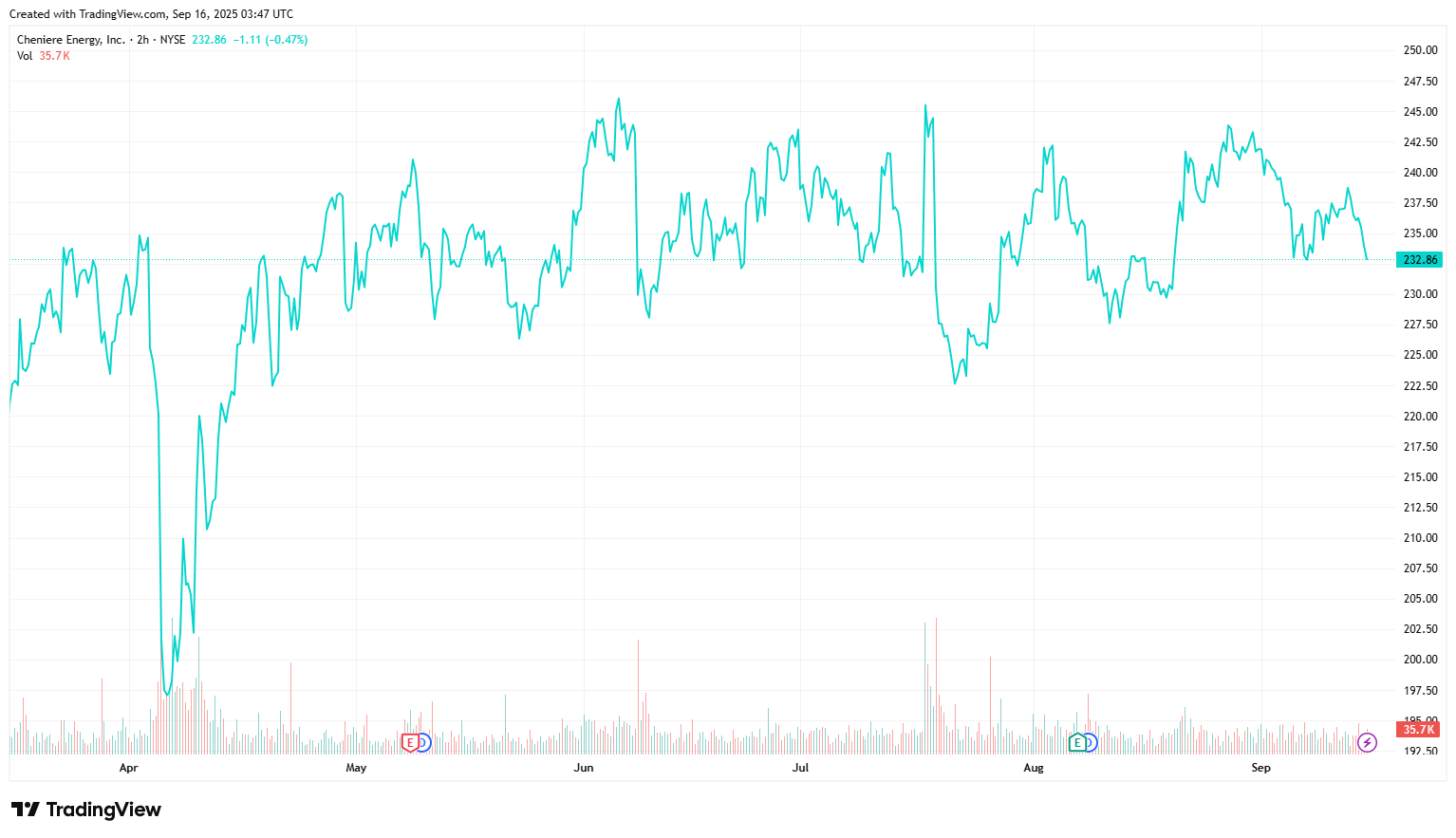

Price Performance

Growth Potential

- Market leadership with the company remaining the largest U.S. LNG exporter (dominant facilities at Sabine Pass and Corpus Christi are being expanded with Stage 3 trains already delivering LNG and aiming to increase output by ~90 mtpa by end of decade), benefiting from high operating leverage and scale advantages with deep-water access, integrated pipeline systems and multi-decade export licenses.

- Strong contractual cashflows with ~85-99 % of volumes under long-term (most extending to 2040s), fixed/variable-fee (indexed to Henry Hub + liquefaction fee or fixed tolling fee) contracts, insulating earnings from spot-price volatility.

- Robust shareholder returns with the company having repurchased ~10% of its outstanding shares since announcing its 2020 vision plan in September 2022 (including ~13.8m shares for ~$2.3bn in 2024) with ~$3bn remaining on the current buyback authorization through 2027, and the Board remaining committed to growing its dividend by ~10% annually through the end of this decade (has been increased by >50% since its initiation in 2021), targeting a payout ratio of ~20% over time.

- Positive LNG market tailwinds with global demand for LNG expected to grow from ~420 mtpa in 2024 to ~650 mtpa by 2030, led by coal-to-gas switching in Asia, energy security concerns in Europe post-Russia war and increased demand for sustainable clean energy (solar/wind provide uncertainty) for datacentres/AI.

- Balance sheet deleveraging (debt reduced by ~$7bn since 2021) which has seen Fitch/Moody/S&P upgrade the credit ratings to BBB/Baa2/BBB, enhancing refinancing flexibility and lowering cost of capital.

Key Risks

- Any oversupply in the market (meaningful supply expected in 2026-28) could see spot prices fall below the company’s marginal cost on uncontracted volumes leading to weaker EBITDA growth and lower netbacks.

- High leverage and interest sensitivity with ~$22.8bn in long-term debt with rising interest rates or project disruptions potentially straining finances.

- Significant change at the senior management level (divisional CEOs).

- Project execution and cost overruns on Corpus Christi (Stage 3).

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

Speak to an Advisor