US CPI Results

October US CPI was 7.7% y/y (previously 8.2%, expected 7.9%) and core US CPI was 6.3% y/y (previous 6.6%).

US inflation ended up lower in October, with smaller than expected price increases for both the total and core measures. These inflation results will mean the Fed will begin to shift its focus from sticky and elevated inflation to developments in the economy and the labour market.

This rings true, especially upon consideration of the US unemployment rate (3.7% Oct'22) which is up from its 29-month low of 3.5%. Such a rate sits outside the target 4% level of the Fed. The face that unemployment has been narrow (between 3.5% and 3.7%) since March suggests a tight labour market which in turn is contributing to causing inflationary pressures.

The low reading of inflation will ease the pressure on the Fed to continue to tighten monetary policy and will give the Fed more leeway to react to any signs of a slowdown in the real economy and the labour market. However, the battle is not over. The market has already formed an expectation that a 50bps increase at the December meeting is probable as the Fed is coming to the tail-end of its rail hikes.

This was reinforced by the chief US economist at Morgan Stanley, Ellen Zentner:

"Policymakers have indicated... a step down to a 50bp rate increase at the December FOMC. Signs of deceleration will help Fed officials moderate the reduction in the pace of tightening, though a stronger than expected December payroll print (300k+) could still complicate the issue at the margin."

Easing supply chains

The core measures showed the smallest price increase since the fall of 2021 (Oct'22 +0.27% m/m vs +0.25% in Sep'21). Prices on core goods (excluding food and energy) declined by 0.4% m/m. Falling prices on sued cars at -2.4% was the main driver. Moreover, core good prices in ex-used cars were up a mere 1% which was the smallest monthly increase since Feb'21. This is a further indication that easing supply chain problems and possibly also declining margins are translating to normal development for good prices.

Declining prices on medicare care (-0.6% m/m) and airline fares (-1.1%) contributed to a slowdown in the monthly price increases for services ex-energy to 0.5% m/m from 0.8% m/m.

Neutral for shelter

Shelter remains the main driver for services inflation, but the monthly increase was almost unchanged compared to the previous month (0.751% vs Sep 0.748%). The weight of rents in the Fed's favoured pCE measure is less than half of that in the CPI which means that we will see even more of a slowdown in that measure.

Slower than expected price increases for food (+0.6% vs a market expectation of 0.7%) and energy (1.8% vs a market expectation of 2.3%) contributed to downside surprise for total CPI.

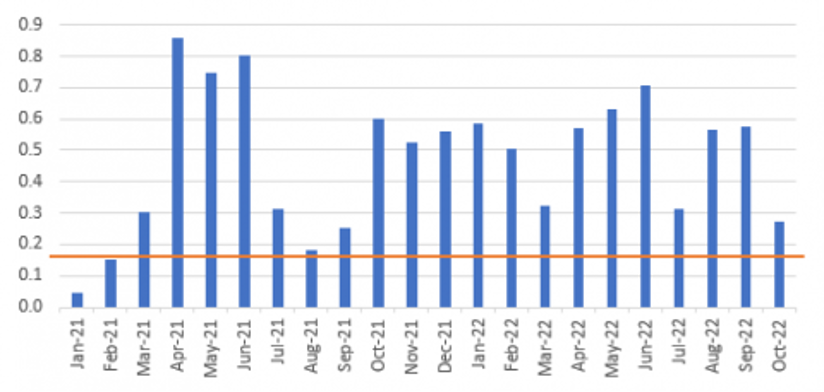

Inflation needs further reduction

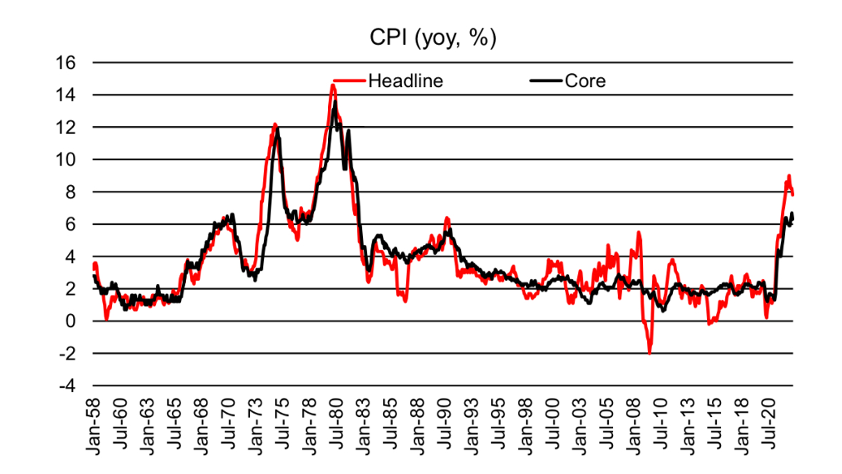

While inflation data is all around positive, the US economy is still well above the 0.17% m/m prints, so there is still more work to be done for it to reach the 2% y/y target. This is seen in Figure 1 wherein the orange line indicates the rate required to achieve 2% y/y over time. Notably, US inflation remains at levels not seen since the 1980s (see Figure 2 below). Thus, the Fed is left to continue to hike rates as inflation remains well above the target amid a growing economy with a tight jobs market.

Information surrounding the November jobs report (released on the 2nd of December) and the November CPI report (13 December) ahead of the FOMC meeting. This reinforces the likelihood of a 50bps interest rate rise, especially considering the spending associated with Christmas and the build-up to New Year's Eve.

All things considered; US inflation data delivered a positive surprise for the market. There is a clear slowdown for core good prices, slowing service inflation, and encouraging signs like the unemployment rate which is closer to its target level. However, the market can continue to expect Hawkish rhetoric over the coming weeks. Inflation is yet to be defeated and therefore the Fed will continue with its Hawkish stance.

To keep up with the latest finance, tech, crypto and geopolitical news, subscribe to our mailing list.

[Disclaimer: The material across our site is provided for informative purposes only and does not contain investment advice.]

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

Speak to an Advisor