Stock Spotlight: Telstra Group Limited (ASX:TLS)

This week's Stock Spotlight is ASX-listed Telstra Group Limited.

About Telstra Group Limited.

Telstra Group Limited provides telecommunications and information services in Australia and internationally. The company operates through six segments: Telstra Consumer; Telstra Business; Telstra Enterprise Australia; Telstra International; Networks, IT and Products; and Telstra InfraCo. It offers telecommunication and technology products and services to consumer and small and medium business customers using mobile and fixed network technologies, as well as operates call centers, retail stores, distribution network, digital channels, distribution systems, and Telstra Plus customer loyalty program. The company also provides network capacity and management, unified communications, cloud, security, industry solutions, integrated and monitoring services to government and large enterprise and business customers; wholesale services, including voice and data; and telecommunication products and services to other carriers, carriage service providers, and internet service providers, as well as builds and manages digital platforms. In addition, it operates the fixed passive network infrastructure, including data centers, exchanges, poles, ducts, pits and pipes, and fiber network; provides wholesale customers with access to network infrastructure; offers long-term access to components of infrastructure under the infrastructure services agreement; and operates the passive and physical mobile tower. The company was formerly known as Telstra Corporation Limited and changed its name to Telstra Group Limited in November 2022. Telstra Group Limited was founded in 1901 and is based in Melbourne, Australia.

Source: EODHD

Key Stats

Key Stats

Source: EODHD. Data as of 22/04/26.

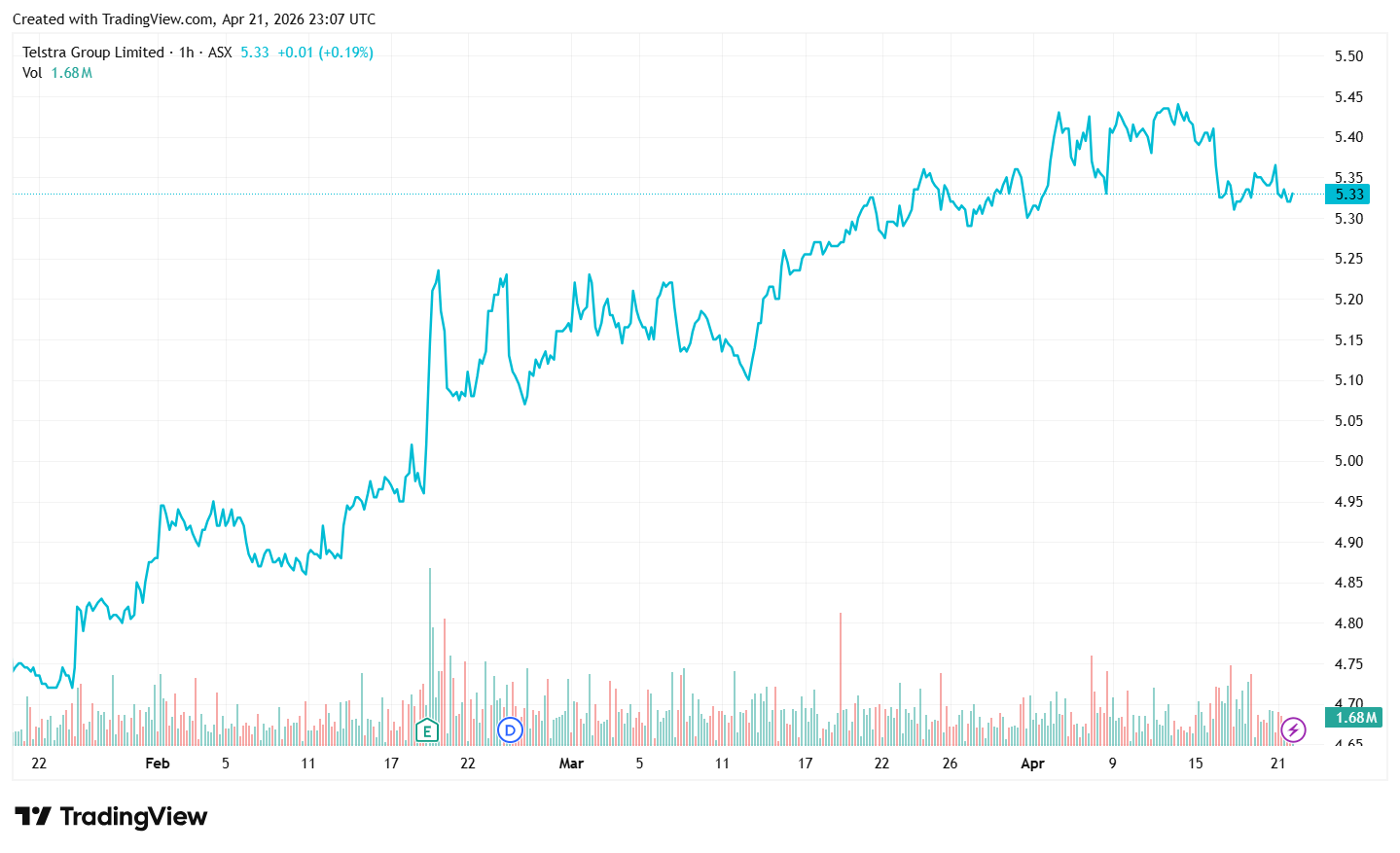

Price Performance

Growth Potential

- TLS is trading largely in line with our revised valuation.

- TLS commands very strong market share position in both Australian mobile and broadband market, with market share of over 30% in both segments.

- Solid FY26 guidance with expected y/y growth in underlying EBITDA.

- Strong market position in mobile which continues to see positive price growth – this is the largest contributor to revenue and earnings.

- Ongoing improvement in the balance sheet position (leverage) provides optionality (e.g. capital management initiatives).

- Attractive free cash flow profile which should be supportive of dividend policy and growth.

- Over the long-term, the introduction of 6G provides potential growth, however we continue to monitor the ROIC from the capex spend.

- Industry consolidation leading to improved pricing behavior by competitors.

Key Risks

- Potential cuts to dividends.

- Deterioration in the core mobile.

- Management fails to deliver on cost-out targets.

- Any increase in churn, particularly in its Mobile segment - worse than expected decrease in average revenue per users (or any price war with competitors).

- Any network disruptions/outages.

- More competition in its Mobile segment. Mergers in Australia creates a better positioned (financially and resource wise) competitor.

- Trading at elevated PE multiple relative to long-term average.

- Investment in 6G infratstructure.

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

Speak to an Advisor