Stock Spotlight: Alphabet Inc (NASDAQ:GOOGL)

About Alphabet Inc

Alphabet Inc. offers various products and platforms in the United States, Europe, the Middle East, Africa, the Asia-Pacific, Canada, and Latin America. It operates through Google Services, Google Cloud, and Other Bets segments. The Google Services segment provides products and services, including ads, Android, Chrome, devices, Gmail, Google Drive, Google Maps, Google Photos, Google Play, Search, and YouTube. It is also involved in the sale of apps and in-app purchases and digital content in Google Play and YouTube; and devices, as well as the provision of YouTube consumer subscription services, such as YouTube TV, YouTube Music and Premium, NFL Sunday Ticket, and Google One. The Google Cloud segment offers consumption-based fees and subscriptions for AI solutions, including AI infrastructure, Vertex AI platform, and Gemini enterprise. It also provides cybersecurity, and data and analytics services; Google Workspace that include cloud-based communication and collaboration tools for enterprises, such as Calendar, Gmail, Docs, Drive, and Meet; and other enterprise services. The Other Bets segment sells transportation and internet services. Alphabet Inc. was incorporated in 1998 and is headquartered in Mountain View, California.

Source: EODHD

Key Stats

Key Stats

Source: EODHD. Data as of 13/05/26.

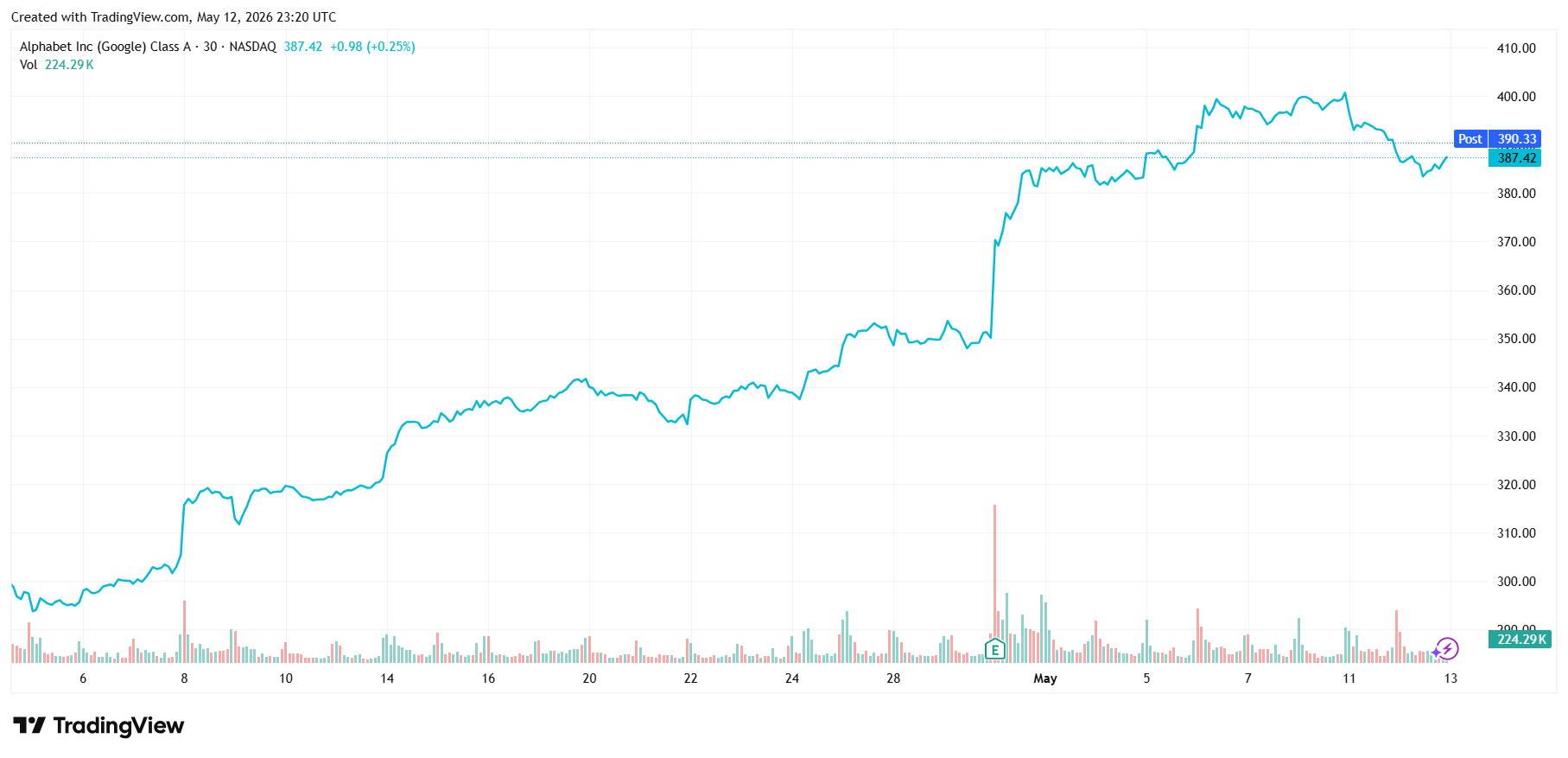

Price Performance

Growth Potential

- Commands a strong market position in online advertising with AI-powered enhancements such as Search AI Overviews now serving over 2bn users/month, boosting engagement and expanding potential monetization for search ads.

- Leveraged to online video streaming and advertising via YouTube.

- Cloud growth and profitability accelerating on AI tailwinds.

- Full‑stack AI leadership provides competitive advantage (developer ecosystem with over 4.4 m developers using Gemini power deep AI integration across Search, ads, Workspace and Cloud + in‑house chip design i.e TPUs such as Ironwood and DeepMind‑powered optimization enables cost‑efficient inference, giving it a competitive infrastructure advantage.

- Long-term potential for valuation upside should any business from Other Bets (Waymo, DeepMind, Verily) mature into material revenue contributors.

- Value accretive acquisitions in existing and new growth areas.

Key Risks

- Threat of increased regulatory scrutiny, including concerns around consumer privacy and personal data.

- Expenses such as TAC (traffic acquisition costs) increase ahead of expectations and which the company is unable to pass onto customers.

- Deterioration in economic conditions, which would put pressure on the advertising revenue.

- Potential return from investment on new, innovative technology fails to yield adequate results.

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.