AI Spending Isn't Slowing. Which Companies Are Really Profiting?

Microsoft, Amazon, Alphabet and Meta have each reaffirmed multi billion dollar commitments to artificial intelligence infrastructure in recent months, even as questions persist about the broader economic outlook. Capital expenditure guidance from all four companies has moved higher rather than lower through 2026, a pattern that runs against the usual approach of pulling back spending when uncertainty rises.

The scale of investment is unprecedented. Data centre CapEx by the world's largest technology companies approached USD 400 billion in 2025 and is projected to increase by a further 64% in 2026 to around USD 725 billion, with approximately 75% of that spending directed towards AI infrastructure rather than traditional cloud operations. Looking further ahead, industry estimates suggest that nearly USD 7 trillion of global investment in data centre infrastructure will be required by 2030 to support the current trajectory of AI demand. This represents one of the largest and most sustained corporate investment cycles in modern history.

For investors, the scale of spending raises an obvious question. If hundreds of billions of dollars are flowing into AI each year, where does that money actually end up, and which companies are converting it into durable profit rather than simply riding a narrative? Answering that question requires looking past the handful of household names that dominate headlines and understanding how AI spending actually moves through the economy.

Follow the Money: Who Really Benefits from AI Spending?

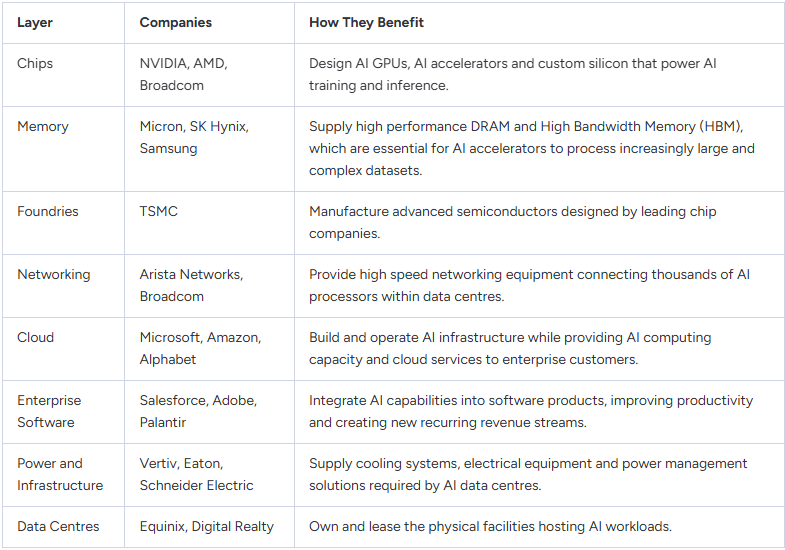

AI spending is not concentrated within a single company or sector. It flows through an interconnected ecosystem, with each layer capturing value by supplying a different component of the AI infrastructure buildout.

Understanding the AI value chain is important because it highlights that the investment opportunity extends well beyond semiconductor designers. An investor who owns only chipmakers gains exposure to one layer of the ecosystem but may miss other beneficiaries, including memory suppliers, networking companies, power and cooling providers, and data centre operators that are also benefiting from the rapid expansion of AI infrastructure. High Bandwidth Memory (HBM), built on advanced DRAM technology, has emerged as one of the most critical components in AI systems. Demand has outpaced supply as increasingly powerful AI accelerators require significantly more high speed memory, creating a supply constraint that many industry analysts expect to persist through at least 2027.

Investors seeking broader exposure to this part of the market, rather than investing in individual memory manufacturers, may also consider thematic funds such as the Roundhill Memory ETF. However, as a relatively small, recently launched and non diversified ETF, it carries a different risk profile from owning the underlying companies directly. Ultimately, understanding where a company sits within the AI value chain, whether in semiconductors, memory, networking, cloud infrastructure or software, is the first step in assessing whether it is likely to benefit directly, indirectly or only marginally from the AI investment cycle.

How to Read an AI Company's Earnings Report

Understanding where a company sits in the AI value chain is only half the picture. Investors also need to assess whether AI is translating into measurable financial performance rather than simply driving headlines. A handful of metrics can help distinguish genuine commercial progress from compelling marketing.

Revenue growth is the starting point, but the figure matters less than its source. Companies frequently reference AI extensively on an earnings call without disclosing what portion of revenue is genuinely attributable to it. Readers should look for AI specific revenue disclosure or a clearly attributed growth contribution, rather than accepting a general reference to AI as the driver behind a strong quarter.

Capital expenditure tells a related but different story. Rising capex can reflect genuine confidence in future AI demand, or it can reflect a company spending defensively to avoid falling behind competitors. The distinction usually comes down to how specifically management can describe the expected return on that spending, and whether capex is growing in line with revenue or running well ahead of it.

Gross margin shows whether AI is actually a profitable line of business yet, or still a cost centre dressed up as a growth story. Many AI linked products carry higher infrastructure and compute costs than the legacy business they sit alongside, and a declining gross margin alongside rising AI revenue can indicate the company is essentially subsidising adoption rather than monetising it.

Free cash flow is where the AI narrative is tested most directly. A company can post accelerating revenue and still burn cash if capital expenditure and infrastructure build out are consuming more than operating cash flow generates. Consistent or improving free cash flow alongside AI growth is a stronger signal than revenue growth on its own.

Management commentary on earnings calls deserves scrutiny for specificity rather than enthusiasm. Vague references to being "well positioned for the AI opportunity" carry little weight. Commentary that references customer counts, contract sizes, deployment timelines or capacity constraints suggests management is speaking from genuine visibility into demand rather than reciting a talking point.

Customer growth is a more concrete adoption signal than product announcements. The number of paying customers, the rate of new customer additions and renewal rates for AI specific products all indicate whether adoption is broadening or concentrated in a small number of early accounts.

Remaining performance obligations (RPO) offer a forward looking view that current period revenue cannot. RPO reflects contracted revenue not yet recognised, and a growing RPO balance tied to AI products signals that demand is being locked in ahead of time rather than assumed. A gap between strong RPO growth and slower recognised revenue growth can also indicate that customers are committing to AI products faster than the company can deliver or recognise the associated revenue.

No single metric tells the full story. Evaluated together, these measures provide a more reliable assessment of whether AI is creating sustainable commercial value or simply generating investor excitement.

Red Flags That Suggest the AI Story May Be Overhyped

Not every company benefiting from AI enthusiasm is actually benefiting from AI economics. A handful of warning signs tend to recur among companies where the story outpaces the substance.

The first is heavy AI marketing paired with minimal AI revenue. When a company's public messaging references AI extensively but its financial disclosures offer little detail on AI specific revenue contribution, the gap itself is informative.

The second is rising spending without clear commercial returns. Capital expenditure that continues to climb without a corresponding improvement in revenue growth, margins or customer metrics suggests the investment may be defensive rather than strategic.

The third is weak customer adoption. Announcements of new AI products or partnerships carry limited weight if usage data, customer counts or renewal figures fail to show meaningful uptake over time.

The fourth is a valuation that assumes unrealistic growth. Some AI linked stocks trade at multiples that require years of uninterrupted, above trend growth to justify. Readers should ask whether the growth priced into the valuation is achievable given the company's current customer base, market size and competitive position.

Where Could the Biggest Opportunities Emerge?

Not every company exposed to the AI investment cycle will benefit equally. The strongest long term opportunities are likely to emerge from businesses with technological leadership, high barriers to entry and products or services that customers cannot easily replace.

GPU designers such as NVIDIA continue to dominate AI training workloads through their integrated hardware, software and developer ecosystems. In memory, suppliers of High Bandwidth Memory (HBM) and advanced DRAM, including SK hynix, Micron and Samsung Electronics, are benefiting from one of the most significant supply constraints in the AI market. Foundries such as TSMC also remain indispensable, as only a handful of manufacturers possess the advanced process technology required to produce leading edge AI chips at scale.

Beyond semiconductors, hyperscalers including Microsoft, Amazon and Alphabet are well positioned through their cloud platforms and expanding AI infrastructure. Companies such as Vertiv, Eaton, Schneider Electric, Equinix and Digital Realty are also benefiting from growing demand for the power, cooling and specialised facilities required to support increasingly complex AI workloads. Enterprise software providers that successfully embed AI into existing products have the potential to generate recurring revenue growth with relatively modest incremental capital investment.

No single company is likely to capture the full economic value created by artificial intelligence. Instead, the most compelling long term opportunities may come from building diversified exposure across the AI value chain, recognising that advances in semiconductors, memory, networking, cloud computing, infrastructure and software are all interconnected. Investors who understand these relationships are better positioned to identify businesses capable of delivering sustainable earnings growth as AI adoption continues to accelerate.

Five Questions to Ask Before Buying an AI Stock

The AI investment opportunity is expanding rapidly, but not every company positioned around the theme will deliver attractive long-term returns. Before investing, it is worth asking a few simple questions:

- Does AI contribute meaningfully to revenue today? Look for evidence that AI is already generating measurable revenue rather than remaining a future opportunity or a marketing initiative.

- Is demand accelerating? Customer growth, enterprise adoption, RPO, and contract wins often provide stronger evidence of future demand than management commentary alone.

- Does management have a clear monetisation strategy? Companies should be able to explain how AI investments will translate into higher revenue, stronger margins or improved cash flow over time.

- Is the business generating sustainable cash flow? Strong free cash flow suggests the company can continue investing in AI while maintaining financial flexibility and reducing reliance on external funding.

- Is the valuation supported by realistic growth expectations? Even exceptional businesses can become poor investments if their share prices already reflect years of uninterrupted growth. Consider whether the company's competitive position and earnings potential justify its valuation.

While no checklist can eliminate investment risk, these questions provide a practical framework for evaluating AI companies using business fundamentals rather than market sentiment.

Final Thoughts

AI spending shows no sign of slowing, and the scale of investment across hyperscalers, infrastructure providers and enterprise software companies suggests this remains an early stage in a much longer buildout. Rapid spending growth does not automatically translate into shareholder value, and not every company positioned near the AI theme will ultimately profit from it.

For investors, the objective is not simply to identify companies talking about AI, but to identify those converting AI investment into sustainable revenue, earnings and cash flow. Understanding where a company sits within the AI value chain, analysing its earnings report critically and applying a disciplined investment framework can help distinguish businesses creating lasting shareholder value from those benefiting primarily from market enthusiasm.

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.