Stock Spotlight: Crowdstrike Holdings Inc (NASDAQ:CRWD)

About Crowdstrike Holdings Inc

CrowdStrike Holdings, Inc. provides cybersecurity solutions in the United States and internationally. Its unified platform provides cloud-delivered protection of endpoints, cloud workloads, identity, and data through a software as a service (SaaS) subscription-based model. The company offers corporate endpoint and cloud workload security, managed security, security and vulnerability management, IT operations management, identity protection, threat intelligence, data protection, SaaS security posture management, and AI powered workflow automation, and securing generative AI workload services, as well as security orchestration, automation, and response; and security information and event management, and log management services. It primarily sells subscriptions to its Falcon platform and cloud modules. The company has a strategic alliance with Cognizant Technology Solutions Corporation to help enterprises secure artificial intelligence across its lifecycle, from the AI agents and models to the foundational infrastructure that supports the entire AI ecosystem. The company was incorporated in 2011 and is headquartered in Austin, Texas.

Source: EODHD

Key Stats

Key Stats

Source: EODHD. Data as of 17/06/26.

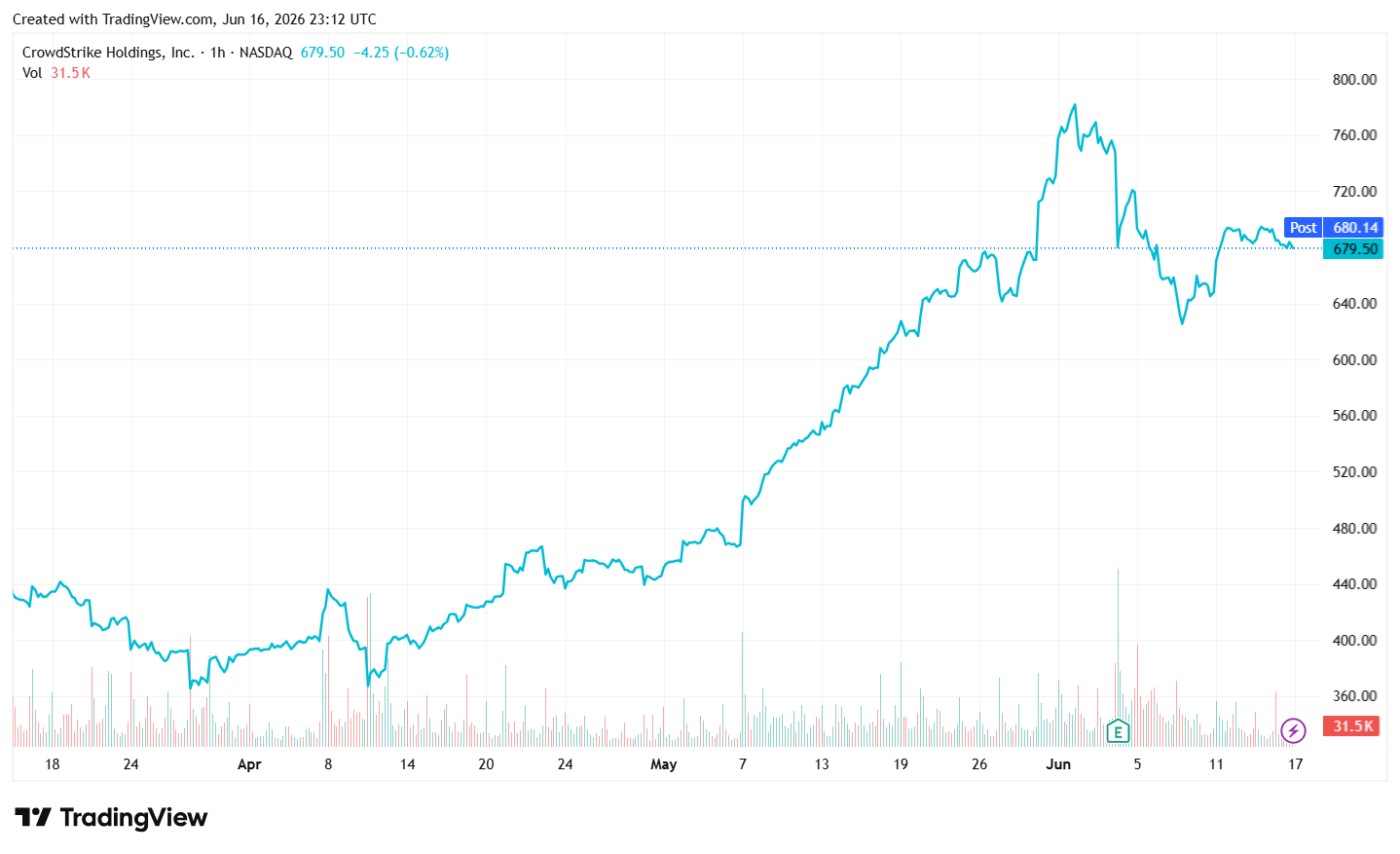

Price Performance

Growth Potential

- AI-native Falcon platform (a unified, cloud-native cybersecurity platform built on AI and behavioral analytics) and data advantage with CRWD having accumulated >2 trillion security events per day, providing one of the richest datasets in cybersecurity. Falcon platform is the best for training security agents as not all data is created equal. CRWD's position at the endpoint gives them access to a trove of high fidelity data, CRWD has a large repository of labeled data from Falcon Complete MDR, CRWD has an extensive threat intelligence database and CRWD's professional services business allows the company to best understand how breaches occur firsthand.

- Large + expanding TAM with global cybersecurity TAM projected to exceed $250bn by 2027 with endpoint, identity, and cloud segments growing fastest. Management expects CRWD’s addressable market (driven by platform expansion) to reach $140bn by 2026.

- Consolidation tailwind - enterprises are increasingly consolidating vendors to simplify security stacks and reduce costs with CRWD’s single-agent architecture and broad module suite making it a natural beneficiary.

- Competitive moat – CRWD’s solutions consistently rank 1 or 2 in Gartner and Forrester evaluations for endpoint and cloud workload protection. CRWD’s low churn (gross retention >98%) and net retention rate consistently above 115% reflect the strong product suite and provides strong cross-sell + upsell opportunities.

- Platform and module expansion beyond core endpoint protection into cloud security, identity protection, SIEM/logs etc. (modular platform of over 26 modules allows cross-selling across security domains) leading to greater wallet share (growth in ARR per customer) and lower churn.

- Secular tailwind of increasing AI threats (as enterprises adopt AI new attack vectors emerge like AI agents, prompt injections and model threats).

- High margin profile and strong FCF generation (management forecast non-GAAP operating margins of >24% and FCF margins >30% by FY27) along with balance sheet strength (~$5bn cash + investments) provide flexibility for M&A and R&D.

Key Risks

- Intensifying competition from Microsoft (Microsoft Defender and Microsoft Sentinel) and Palo Alto Networks.

- Potential enterprise budget tightening in macro slowdowns.

- Regulatory and data privacy risk.

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

Speak to an Advisor