Stock Spotlight: Capstone Copper Corp. (ASX:CSC)

About Capstone Copper Corp.

Capstone Copper Corp., a copper mining company, mines, explores for, and develops mineral properties in the United States, Chile, and Mexico. The company primarily explores copper, silver, gold, molybdenum, zinc, iron, cobalt, and other base metals. Capstone Copper Corp. is headquartered in Vancouver, Canada.

Source: EODHD

Key Stats

Key Stats

Source: EODHD. Data as of 15/07/26.

Price Performance

Growth Potential

- Bull case: The bull case rests on three features: improving portfolio mix toward lower-cost Chilean sulphide tonnes, rising EBITDA and cash generation at current copper prices, and a growth queue that can materially lift production beyond the 2026 guidance plateau into 2027 and later years.

- Geographic diversification: Operating risk is spread safely across established mining jurisdictions in the Americas, mitigating single-jurisdiction exposure. The portfolio includes Mantoverde (70% owned) and Mantos Blancos (100% owned) in Chile, Pinto Valley (100% owned) in the USA, and Cozamin (100% owned) in Mexico.

- Peer-leading project optionality: Capstone provides highly visible growth optionality. The imminent MV-O expansion adds approximately 20,000 tonnes of annual copper capacity, while a 4Q26 Final Investment Decision on the Santo Domingo project unlocks transformational district-scale growth.

- Proven operational execution: The company has a demonstrated track record of delivering continuous improvement, achieving a 37% increase in production over the last three years.

- Positive copper outlook. The global copper market is entering a period of structural supply deficit over the next five to ten years, underpinned by secular demand growth tied to the global energy transition.

- Management quality: Led by a highly experienced executive team—including President & CEO Cashel Meagher, SVP & COO Jim Whittaker, and SVP & CFO Raman Randhawa.

Key Risks

- Bear case: The bear case is that Capstone remains operationally and financially exposed to mine sequencing, labour disruption, input-cost inflation, project execution, and the balance-sheet burden of funding large growth projects in a cyclical commodity business

- Commodity price risk and input cost inflation (higher diesel & sulfuric acid prices).

- Operational risk at Pinto Valley Pinto Valley (continues to face reliability issues).

- Capital expenditure risk with elevated capex across FY26/27.

- Labour disruption risk and jurisdiction risk (operates in Chile, Mexico and U.S.).

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

This week's Stock Spotlight is NYSE-listed Wells Fargo & Company. About Wells Fargo & Company. Wells Fargo & Company, a financial services company, provides diversified banking, investment, mortgage, and consumer and commercial finance products and services in the United States and internationally. It operates through four segments: Consumer Banking and Lending; Commercial Banking; Corporate and Investment Banking; and Wealth and Investment Management. The company's financial products and services includes checking and savings accounts, and credit and debit cards, as well as home, auto, personal, and small business lending services. It also provides personalized wealth management, brokerage, financial planning, lending, private banking, trust and fiduciary products and services; and financial solutions to private, family owned and public companies through products and services including banking and credit products across multiple industry sectors and municipalities, secured lending and lease products, and treasury management. In addition, it offers a suite of capital markets, banking, and financial products and services, such as corporate banking, investment banking, treasury management, commercial real estate lending and servicing, equity, and fixed income solutions, as well as sales, trading, and research capabilities services to corporate, commercial real estate, government, and institutional clients. Wells Fargo & Company was founded in 1852 and is headquartered in San Francisco, California. Source: EODHD Key Stats

This week's Stock Spotlight is NYSE-listed Bank of America Corp. About Bank of America Corp. Bank of America Corporation, through its subsidiaries, provides various financial products and services for individual consumers, small and middle-market businesses, institutional investors, large corporations, and governments worldwide. It operates through four segments: Consumer Banking, Global Wealth & Investment Management (GWIM), Global Banking, and Global Markets. The Consumer Banking segment offers traditional and money market savings accounts, certificates of deposit and IRAs, checking accounts, and investment accounts and products; credit and debit cards; residential mortgages and home equity loans; and direct and indirect loans. The GWIM segment provides investment management, brokerage, banking, and trust and retirement products and services; wealth management solutions; and customized solutions, including specialty asset management services. The Global Banking segment offers lending products and services, including commercial loans, leases, commitment facilities, trade finance, and commercial real estate and asset-based lending; treasury solutions, and underwriting and advisory services. The Global Markets segment provides market-making, financing, securities clearing, settlement, and custody services; securities and derivative products; and risk management products using interest rate, equity, credit, currency and commodity derivatives, foreign exchange, fixed-income, and mortgage-related products. Bank of America Corporation was founded in 1784 and is based in Charlotte, North Carolina. Source: EODHD Key Stats

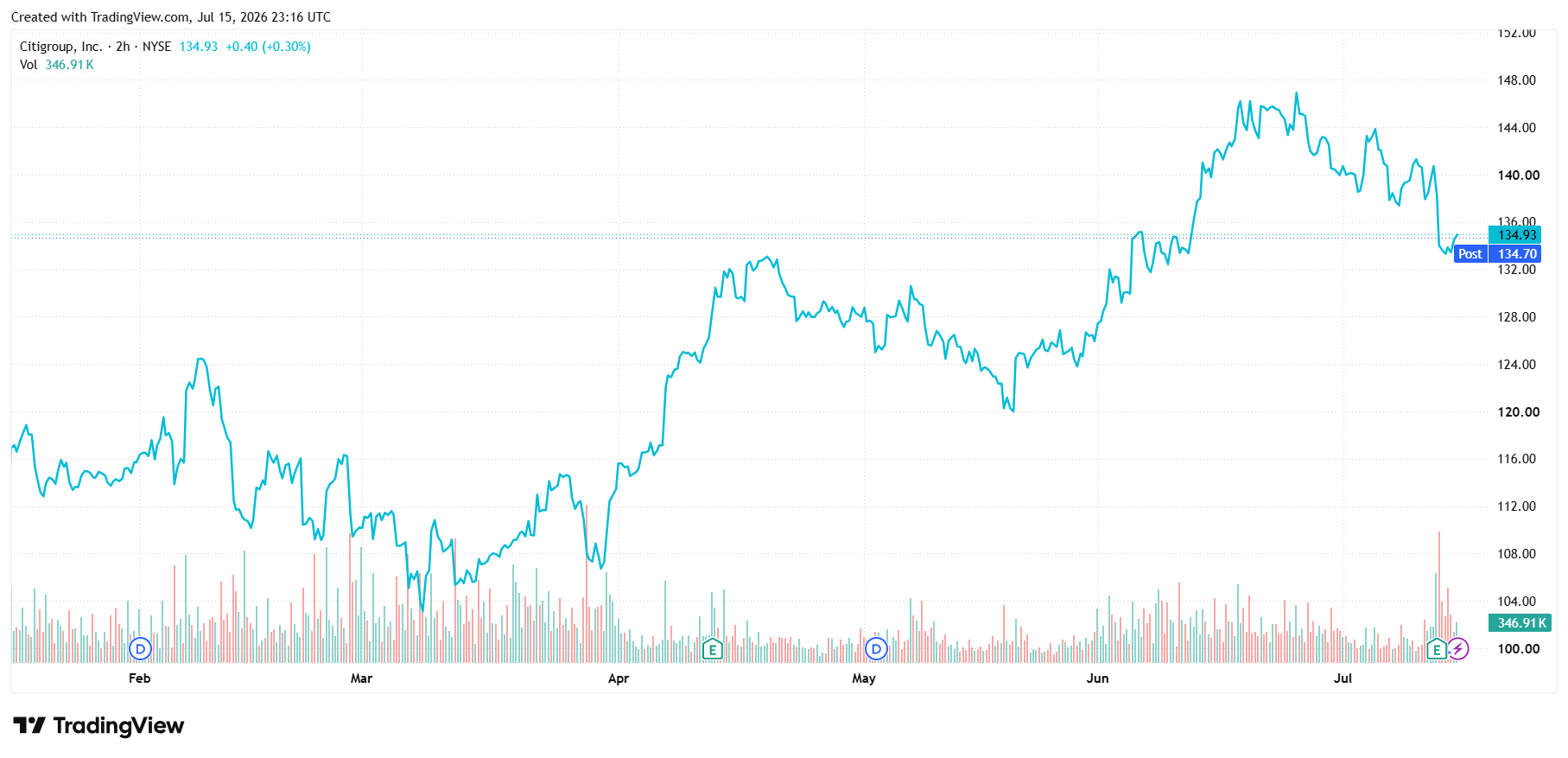

This week's Stock Spotlight is NYSE-listed Citigroup Inc. About Citigroup Inc. Citigroup Inc., a diversified financial service holding company, provides various financial products and services to consumers, corporations, governments, and institutions. It operates through five segments: Services, Markets, Banking, U.S. Personal Banking, and Wealth. The Services segment includes treasury and trade solutions, which provides cash management, trade, and working capital solutions to multinational corporations, financial institutions, and public sector organizations; and securities services, such as cross-border support for clients, local market expertise, post-trade technologies, data solutions, and various securities services solutions. The Markets segment offers sales and trading services for equities, foreign exchange, rates, spread products, and commodities to corporate, institutional, and public sector clients; and market-making services, including asset classes, risk management solutions, financing, and prime brokerage. The Banking segment includes investment banking services comprising equity and debt capital markets-related strategic financing solutions; advisory services related to mergers and acquisitions, divestitures, restructurings, and corporate defense activities; and corporate lending consists of corporate and commercial banking. The U.S. Personal Banking segment provides proprietary and co-branded card portfolios; and traditional banking services to retail and small business customers. The Wealth segment offers financial services to high-net-worth clients through banking, lending, mortgages, investment, custody, and trust product offerings; professional industries, including law firms, consulting groups, accounting, and asset management; and affluent and high net worth clients. The company operates in North America, the United Kingdom, Japan, North and South Asia, Australia, Europe, the Middle East, and Africa. Citigroup Inc. was founded in 1812 and is headquartered in New York, New York. Source: EODHD Key Stats

AI is driving unprecedented demand for data centres. Discover how the infrastructure powering AI is creating opportunities across energy, property and technology.

About Qualcomm Inc. QUALCOMM Incorporated engages in the development and commercialization of foundational technologies for the wireless industry worldwide. It operates through three segments: Qualcomm CDMA Technologies (QCT); Qualcomm Technology Licensing (QTL); and Qualcomm Strategic Initiatives (QSI). The QCT segment develops and supplies integrated circuits and system software with connectivity and computing technologies for use in mobile devices; automotive systems for connectivity, digital cockpit, and ADAS/AD; and IoT, including consumer electronic devices, industrial devices, and edge networking products. The QTL segment grants licenses or provides rights to use portions of its intellectual property portfolio, which include various patent rights useful in the manufacture and sale of wireless products comprising products implementing LTE, and/or OFDMA-based 5G products and derivatives; to use cellular standard-essential patents, including 3G, 4G and 5G for cellular devices. The QSI segment invests in early-stage companies in various industries, including 5G, artificial intelligence, automotive, consumer, enterprise, cloud, IoT, and extended reality, and investments, including non-marketable equity securities and, to a lesser extent, marketable equity securities, and convertible debt instruments. It also provides development, and other services and sells related products to the United States government agencies and their contractors. In addition, the company is also involved in Qualcomm government technologies and data center businesses. Further, it provides security and intelligence services for unmanaged networks through software-based network security solutions. QUALCOMM Incorporated was incorporated in 1985 and is headquartered in San Diego, California. Source: EODHD Key Stats

AI spending is accelerating in 2026. Learn how to read AI earnings, spot overhyped stocks and find companies converting AI investment into real profit.

Wall Street posted its strongest quarter since 2020. Discover what's driving the rally, why the US outperformed the ASX, and what it means for Australian investors.

About Oracle Corporation Oracle Corporation offers products and services that build, run and support enterprise information technology frameworks worldwide. Its Oracle cloud software as a service offering includes various cloud software applications, including Oracle Fusion cloud enterprise resource planning ERP, Oracle Fusion cloud enterprise performance management EPM, Oracle Fusion cloud supply chain and manufacturing management SCM, Oracle Fusion cloud human capital management HCM, and NetSuite applications suite, Oracle Health applications, as well as Oracle Fusion Sales, Service, and Marketing. The company also offers cloud-based industry solutions for various industries; Oracle cloud license and on-premise license; and Oracle license support services. In addition, it provides cloud and license business' infrastructure technologies, such as the Oracle Database and MySQL Database; Java, a software development language; and middleware, including development tools and others. The company's cloud and license business' infrastructure technologies also comprise cloud-based compute, storage, and networking capabilities; and Oracle autonomous database, as well as AI, Internet-of-Things, machine learning, digital assistant, and blockchain. Further, it provides hardware products and other hardware-related software offerings, including Oracle engineered systems, enterprise servers, storage solutions, industry-specific hardware, virtualization software, operating systems, management software, and related hardware support services, and consulting and advanced customer services. It markets and sells its cloud, license, hardware, support, and services offerings directly to businesses in various industries, government agencies, and educational institutions, as well as through indirect channels. Oracle Corporation has a strategic alliance with Metron, Inc. The company was founded in 1977 and is headquartered in Austin, Texas. Source: EODHD Key Stats

About HDFC Bank Limited HDFC Bank Limited provides banking and financial products and services to individuals and businesses in India, Bahrain, Hong Kong, Singapore, and Dubai. The company operates through Treasury, Retail Banking, Wholesale Banking, Other Banking Business, Insurance Business, and Other segments. It offers savings, salary, current, rural, public provident fund, pension, and demat accounts; fixed and recurring deposits; and safe deposit lockers, as well as offshore accounts and deposits, and overdrafts against fixed deposits. The company also provides personal, home, car, two-wheeler, business, doctor, educational, gold, consumer, and rural loans; loans against properties, securities, mutual funds, rental receivables, and assets; loans for professionals; government sponsored programs; and loans on credit card, as well as working capital and commercial/construction equipment finance, healthcare/medical equipment, commercial vehicle finance, dealer finance, and term loans. In addition, it offers credit, debit, prepaid, forex, and kisan gold cards; payment and collection, export, import, remittance, bank guarantee, letter of credit, trade, hedging, and merchant and cash management services; and insurance and investment products. Further, the company provides short term finance, bill discounting, structured finance, export credit, loan repayment, custodial, and documents collection services; online, mobile, and phone banking services; unified payment interface, immediate payment, national electronic funds transfer, and real time gross settlement services; channel financing, vendor financing, reimbursement account, money market, derivatives, employee trusts, cash surplus corporates, tax payment, and bankers to rights/public issue services; and financial solutions for supply chain partners and agricultural customers. It operates branches and automated teller machines in various cities/towns. The company was incorporated in 1994 and is headquartered in Mumbai, India. Source: EODHD Key Stats

About Woodside Energy Group Woodside Energy Group Ltd engages in the exploration, evaluation, development, production, marketing, and sale of hydrocarbons in the Asia Pacific, Africa, the Americas, and the Europe. It produces liquefied natural gas, pipeline gas, crude oil and condensate, and natural gas liquids. The company holds interests in the Pluto LNG, North West Shelf, Wheatstone and Julimar-Brunello, Bass Strait, Ngujima-Yin FPSO, Okha FPSO, Pyrenees FPSO, Macedon, Shenzi, Mad dog, Greater Angostura, as well as Scarborough, Sangomar, Trion, Calypso, Browse, Liard, Ruby, Sangomar, Atlantis, Woodside Solar opportunity, and Sunrise and Troubadour. It is also involved in the development of new energy products and lower-carbon services. The company was formerly known as Woodside Petroleum Ltd and changed its name to Woodside Energy Group Ltd in May 2022. Woodside Energy Group Ltd was founded in 1954 and is headquartered in Perth, Australia. Source: EODHD Key Stats