Stock Spotlight: Citigroup Inc (NYSE:C)

This week's Stock Spotlight is NYSE-listed Citigroup Inc.

About Citigroup Inc.

Citigroup Inc., a diversified financial service holding company, provides various financial products and services to consumers, corporations, governments, and institutions. It operates through five segments: Services, Markets, Banking, U.S. Personal Banking, and Wealth. The Services segment includes treasury and trade solutions, which provides cash management, trade, and working capital solutions to multinational corporations, financial institutions, and public sector organizations; and securities services, such as cross-border support for clients, local market expertise, post-trade technologies, data solutions, and various securities services solutions. The Markets segment offers sales and trading services for equities, foreign exchange, rates, spread products, and commodities to corporate, institutional, and public sector clients; and market-making services, including asset classes, risk management solutions, financing, and prime brokerage. The Banking segment includes investment banking services comprising equity and debt capital markets-related strategic financing solutions; advisory services related to mergers and acquisitions, divestitures, restructurings, and corporate defense activities; and corporate lending consists of corporate and commercial banking. The U.S. Personal Banking segment provides proprietary and co-branded card portfolios; and traditional banking services to retail and small business customers. The Wealth segment offers financial services to high-net-worth clients through banking, lending, mortgages, investment, custody, and trust product offerings; professional industries, including law firms, consulting groups, accounting, and asset management; and affluent and high net worth clients. The company operates in North America, the United Kingdom, Japan, North and South Asia, Australia, Europe, the Middle East, and Africa. Citigroup Inc. was founded in 1812 and is headquartered in New York, New York.

Source: EODHD

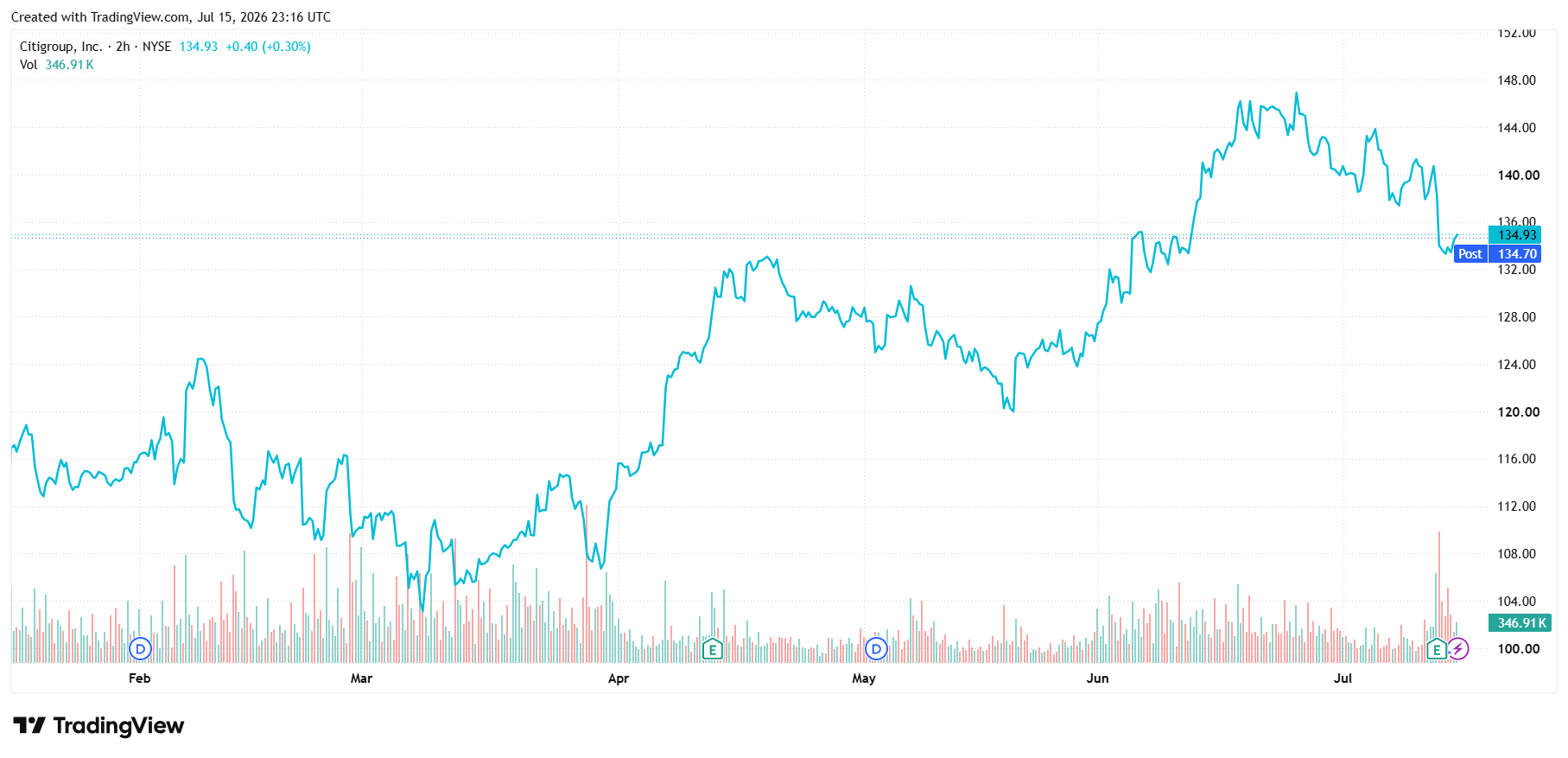

Key Stats

Key Stats

Source: EODHD. Data as of 16/07/26.

Price Performance

Growth Potential

- Multi-year RoTCE re-rating path with management guiding for 11-13% RoTCE in both 2027 and 2028 (near-term), trending toward the higher end by 2028, and 14-15% over the medium term (2029–2031), up from 7.7% (8.8% ex-notable items) in 2025.

- AI-driven productivity with AI code-review tools freeing ~100,000 engineering hours/week, developer productivity gains up +40%, and agentic AI being scaled bank-wide for growth (new products), operations (KYC, reconciliations) and risk/fraud defense.

- Transformation program near completion with 90% of remediation/transformation programs at or near target state as of 1Q26, which is progressively removing “billions of dollars” of "stranded costs" and freeing capacity for reinvestment with management forecasting efficiency ratio (non-interest expenses ÷ total revenue i.e operating cost spend to generate a single dollar of revenue) to fall from 65% (2025) to 55-60% in the near-term (2027-2028) and <55% in the medium-term (2029-2031).

- Capital return acceleration with the Board announcing a new $30bn buyback authorization (on top of prior $20bn program of which $19.6bn has been executed with the bank having returned ~$45bn since 2022) and forecasting buybacks to be higher in 2026 vs 2025, funded by a combination of organic capital generation, DTA utilization and an improving stress capital buffer.

- DTA utilization with continued U.S. profitability improvement expected to unlock further deferred tax asset value, directly improving capital productivity and medium-term returns.

- Segment-specific growth engines with Wealth targeting low-teens revenue CAGR and >20% RoTCE medium-term (vs negative in 2023 and 8% in 2025 by capturing $5 trillion held-away asset opportunity from own current client base), Markets Equities scaling via Prime Brokerage (balances doubled from $200bn to $450bn since 2022), Commercial Banking targeting a $100bn addressable wallet (bank is still ~1/3 the size of market leaders) and Investment Banking seeing increasing wallet share (up +70bps vs 2022 to 4.7% in 2025) driven by improving incumbency with financial sponsors (share up +135bps to highest in a decade).

Key Risks

- Interest rate/macro risk with a significant share of NII (Services deposit spread income, Wealth/USCC lending) sensitive to Fed policy.

- Regulatory overhang with the bank remaining under multi-year (2020-origin) regulatory consent orders related to risk data aggregation, controls and governance with management noting the timing of their removal “sits with regulators” and not in their control.

- Competitive scale gap (especially in Equities/Prime and Wealth) with peers like JP Morgan/Morgan Stanley/BofA having multi-year platform and balance-sheet head start.

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.