Strike, Pause, Denial: Inside the Trump–Iran Five-Day Window

The most consequential market event of the past week was not a central bank decision, an earnings release, or an economic data print. It was a social media post published before dawn on Monday morning.

At a time when regional leaders and global markets were positioned for escalation, President Trump signalled a pause in planned strikes on Iran’s power infrastructure, citing progress in negotiations. The market response was immediate and pronounced. Brent crude, which had traded above USD112 per barrel late the previous week, fell by close to 11% to below USD100 within a single session, while US equity futures rallied sharply. Within hours, however, Iran’s Parliament Speaker rejected the existence of any negotiations and accused the US of attempting to influence financial and energy markets, undermining the credibility of the initial announcement.

Markets subsequently retraced part of the move as uncertainty intensified. Oil remained lower and equities retained some gains, but conviction weakened as investors were left without a consistent narrative to anchor expectations. This is not an isolated dislocation but a reflection of a broader shift toward strategic ambiguity, where market direction is shaped by conflicting signals and limited visibility. The five-day window does not represent a diplomatic breakthrough. It is a period in which markets must continuously recalibrate competing scenarios in real time, with asset prices increasingly driven by shifting probabilities and their implications for inflation, interest rates, and valuations.

What Actually Happened: From Ultimatum to Five-Day Window

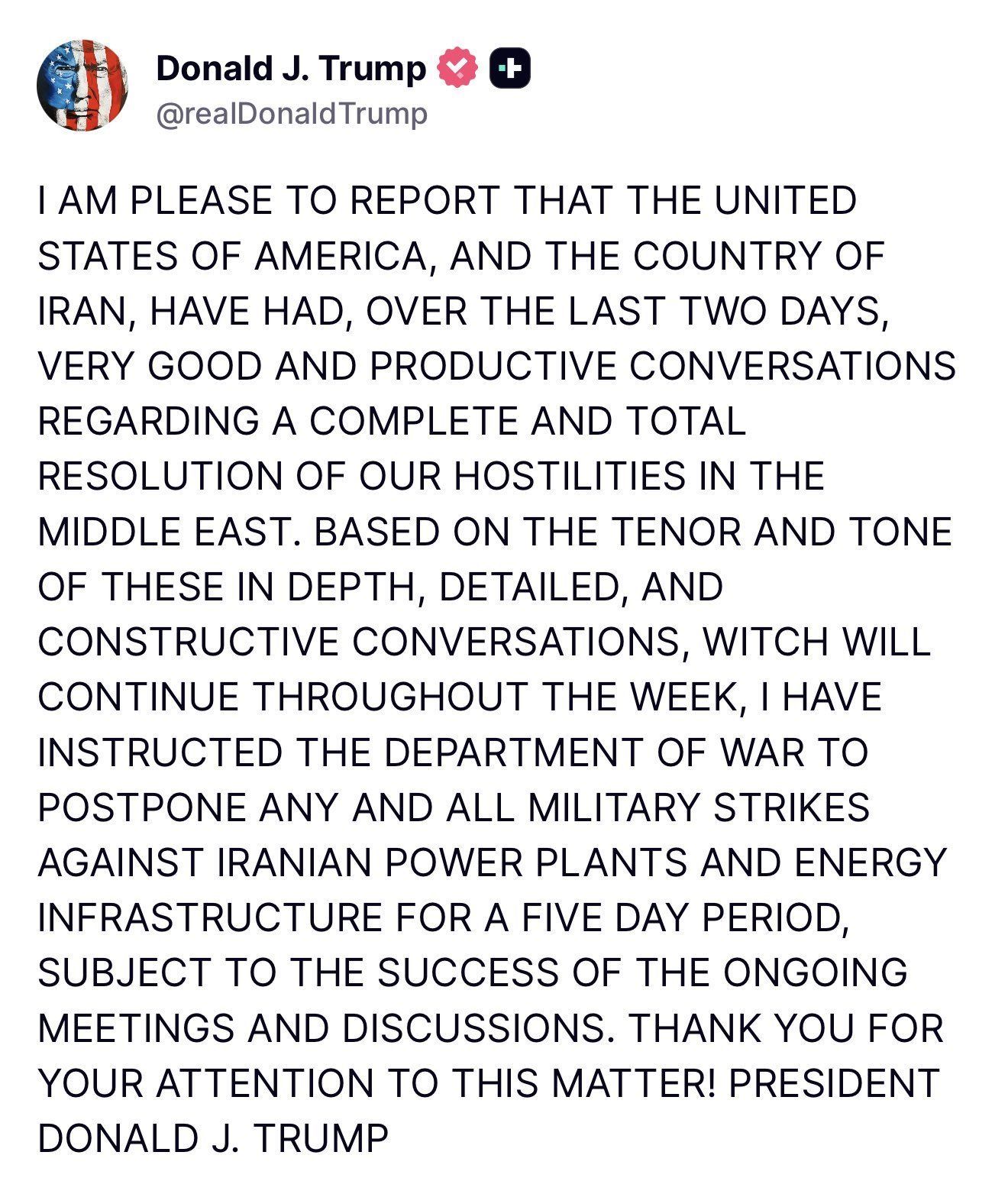

Over the weekend, President Trump issued a 48-hour ultimatum, warning of strikes on Iran’s power infrastructure if shipping through the Strait of Hormuz was not restored. The deadline was set to expire Monday evening, Washington time, with markets positioned for imminent escalation. In parallel, US envoys were reported to have engaged in indirect communications with senior Iranian officials, including Parliament Speaker Mohammad Bagher Ghalibaf, a key figure within Iran’s decision-making structure.

Shortly thereafter, President Trump announced that “very good and productive” discussions had taken place and ordered a five-day postponement of planned military action. Iran’s response was immediate but measured. Officials acknowledged messages conveyed through intermediary countries, confirming backchannel activity, while firmly denying any direct negotiations. The comments were dismissed as psychological pressure, with suggestions that the appearance of diplomacy may be intended to support ongoing military positioning.

At the same time, Israeli leadership signalled that military operations would continue alongside diplomatic efforts, reinforcing the dual-track nature of the current strategy. These parallel developments are not contradictory. They reflect a coordinated approach in which military pressure and diplomatic signalling operate simultaneously, leaving markets to interpret a policy framework that is deliberately fluid and strategically ambiguous.

The extension from a 48-hour deadline to a five-day window materially alters the structure of risk. What was initially a binary event has become a rolling period of uncertainty, where outcomes remain fluid and highly sensitive to incremental developments. This shift introduces the potential for repeated narrative reversals, with each headline capable of triggering rapid repricing across asset classes. A growing credibility gap between conflicting signals further reduces the reliability of official messaging, increasing the risk of mispricing as markets attempt to distinguish between genuine policy direction and strategic posturing.

Why Markets Reacted So Violently: Relief Rally Meets Reality

The sharp intraday swing in Brent crude was not irrational. It reflected a rapid repricing of a binary risk event under conditions of genuine uncertainty. At the time of the announcement, markets had already embedded a meaningful Strait of Hormuz risk premium in oil prices, reflecting the probability of supply disruption. The signal of a delay implied that this premium could be unwound, triggering an immediate and mechanical response. Brent crude fell by close to 11% while equity futures rallied, as traders moved quickly to reduce defensive positioning and price out near-term escalation risk.

This initial relief, however, was driven more by positioning than by any fundamental shift in the underlying outlook. As the implications of the five-day window became clearer, markets began to retrace. Oil stabilised and partially rebounded, while equity gains faded. The reversal highlighted a critical point. The delay did not remove risk but redistributed it across time, extending uncertainty rather than resolving it.

When Iran denied that negotiations were taking place, only part of the previously unwound risk premium was reinstated. This partial reversal is instructive. Markets assigned some credibility to both narratives, settling on an outcome that reflected reduced near-term escalation risk without fully discounting the possibility of renewed tensions. In this environment, price action is increasingly shaped by short-term information flow rather than stable fundamentals. With limited macroeconomic data to anchor expectations, each headline has the potential to trigger rapid repricing. For investors, this reinforces the importance of scenario-based positioning over reactive trading, as the speed and reversibility of market moves make it difficult to respond consistently to each development.

Three Scenarios: What the Five-Day Window Could Produce

Within this compressed five-day window, markets are effectively running a continuous scenario analysis.

Scenario 1: Diplomatic Progress

A framework agreement emerges through backchannel intermediaries, supported by ongoing engagement from regional actors. Iran agrees to a partial reopening of the Strait of Hormuz in exchange for ceasefire assurances and some form of sanctions relief. Under this scenario, Brent crude retraces toward USD80–85 per barrel as supply disruption risks ease. Central banks face reduced inflation pressure, potentially removing the need for further tightening. Rate-sensitive sectors such as REITs, consumer discretionary, and technology would likely benefit from improved sentiment and lower yields. Conversely, energy equities could give back a portion of recent gains. This represents the most constructive outcome for broader markets but a less favourable environment for concentrated energy exposures.

Scenario 2: Stalemate – Talks Without Resolution

The most probable outcome given the divergence in public positions. The pause extends informally, with neither clear escalation nor meaningful progress toward resolution. Oil prices remain elevated in the USD90–100 range, reflecting ongoing supply constraints without a full disruption. Markets remain range-bound and highly sensitive to incremental developments, with volatility structurally elevated. Policymakers continue to signal openness to diplomacy while preserving optionality for further action. This environment supports a balanced but cautious approach, with continued exposure to energy, gold, and shorter-duration fixed income.

Scenario 3: Breakdown and Military Escalation

Diplomatic efforts fail and tensions escalate into direct military action, including potential strikes on Iranian infrastructure. A significant disruption to energy flows drives oil prices above USD120–130 per barrel, intensifying global inflation pressures. Central banks are forced to maintain or reintroduce tightening bias despite weakening growth conditions, increasing recession risk across developed economies. In this scenario, defensive positioning becomes critical, with a preference for energy exposure, gold, and higher cash allocations as markets adjust to a more severe macro and geopolitical shock.

Market Signals Under Stress: What Markets Are Telling You Right Now

Current market behaviour provides a clear lens into how these probabilities are being interpreted across asset classes.

Oil remains the primary transmission mechanism, with price action characterised by sharp swings driven by headline risk rather than stable conviction. Markets continue to reprice supply disruption scenarios in real time, reinforcing volatility across energy markets.

Equity markets are balancing two competing forces. On one hand, geopolitical escalation and rising oil prices are weighing on sentiment and driving capital outflows. On the other, intermittent rallies reflect positioning adjustments tied to shifting expectations around inflation and interest rates. As a result, equity performance has been volatile rather than directionally decisive.

Bond markets are delivering a more conflicted signal. Yields initially moved higher in response to inflation risks stemming from energy prices, but have since shown periods of stabilisation as growth concerns begin to surface. This tension highlights an unresolved market debate between inflation persistence and potential demand destruction.

Gold has diverged from its traditional role as a safe-haven asset, experiencing a sharp decline during the height of the recent escalation. The move reflects the dominance of rising real yields and US dollar strength over defensive demand. While prices have shown signs of stabilisation more recently, the broader trend underscores a shift in market dynamics where macro factors are overriding conventional geopolitical hedging behaviour.

Meanwhile, the US dollar has strengthened, reflecting a clear preference for liquidity and defensive positioning. Capital flows into the dollar continue to reinforce tighter global financial conditions.

Taken together, these signals point to a market that is not purely risk-off, but one that is being driven by an inflation-led shock, with cross-asset relationships behaving in less predictable ways.

Positioning in a Headline-Driven Market

In an environment where a single social media post can move oil by 12% and equity futures by 3% within minutes, and where such volatility reflects a deliberate feature of policy rather than a temporary distortion, conventional portfolio construction frameworks require reassessment. A warfare portfolio is not a short-term crisis allocation designed to absorb a transient shock. It is a portfolio deliberately structured to operate in a regime where geopolitical binary risk is persistent and embedded within the investment landscape.

The core principles underpinning this approach are consistent across all three scenarios outlined above.

Energy exposure functions as a structural hedge rather than a purely directional commodity position. Companies such as Woodside and Santos are generating strong revenues in an elevated oil price environment, supporting robust cash flow and dividend profiles that provide resilience across outcomes. In a de-escalation scenario, some gains may unwind, but underlying LNG demand into a structurally constrained Asian market remains supportive. In an escalation scenario, these names are among the most direct beneficiaries within the ASX.

Gold retains a role as a conflict hedge rather than a simple rate-sensitive asset. Its recent decline reflects a mechanical adjustment to rising real yields rather than a deterioration in its strategic function. The underlying conflict premium remains intact and is likely to reprice quickly in a scenario where escalation places simultaneous pressure on both equities and fixed income markets.

Duration management within fixed income represents one of the most effective levers available to investors. The transmission mechanism from oil to inflation and subsequently to interest rates remains highly responsive to developments in the Strait. In this context, shorter-duration and floating-rate exposures offer greater resilience than long-duration bonds across a range of potential outcomes.

Reducing exposure to consumer discretionary sectors is a positioning decision that holds across scenarios. Elevated fuel costs, recent RBA tightening, and persistent cost-of-living pressures continue to constrain household spending. While a diplomatic resolution may stabilise conditions, it is unlikely to reverse these pressures in the near term.

Maintaining a cash allocation should be viewed as a strategic decision rather than a conservative one. In a market characterised by binary outcomes, liquidity carries option value. It preserves the flexibility to deploy capital as conditions evolve, rather than being constrained by positions established under a different set of assumptions.

Conclusion: Uncertainty as a Structural Market Condition

The five-day window will close. What will remain is the broader regime of geopolitical uncertainty that the Iran conflict has introduced into global markets. Strategic unpredictability is not a temporary phase in negotiations but an enduring feature of the current policy environment. Portfolios constructed on the assumption that clarity is imminent risk being misaligned with a market that continues to operate without a stable narrative.

In this context, the investors best positioned are not those attempting to predict whether a resolution is reached by 28 March. Rather, they are those who structure portfolios to participate in upside scenarios while remaining resilient to downside outcomes, without relying on a single path to materialise. This approach recognises that volatility is not episodic but embedded in the current regime.

As noted by market participants, sustained relief in asset prices will require tangible geopolitical progress. Until such confirmation emerges, uncertainty should not be viewed solely as a risk to be eliminated. It is a structural condition that must be actively managed. Portfolio construction frameworks designed for asymmetric outcomes and rapid repricing are therefore essential in navigating an environment defined by persistent geopolitical tension. For a detailed view of how we position for this environment, click

here to access our Wartime Portfolio.

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

Speak to an Advisor

As AI becomes cheaper to deploy, could the next investment winners shift beyond chipmakers? Explore how the AI cost race is redefining future tech leaders.

Get the latest on Santos Limited (ASX:STO), including stock performance, technical analysis, forecasts & key insights. See if STO supports your goals.

Big Tech earnings could shake your portfolio this week. Understand how the latest results may influence global markets, the ASX and your investment strategy.

A second strategic chokepoint is under threat after Hormuz. Discover how the Bab al-Mandeb blockade could affect oil prices, inflation, interest rates and your portfolio.

This week's Stock Spotlight is NYSE-listed JPMorgan Chase & Co. About JPMorgan Chase & Co. JPMorgan Chase & Co. operates as a bank and financial holding company in the United States, rest of North America, Europe, the Middle East, Africa, the Asia Pacific, Latin America, and the Caribbean. It operates in three segments: Consumer & Community Banking, Commercial & Investment Bank, and Asset & Wealth Management. The company offers deposit, investment and lending products, and cash management; mortgage origination and servicing activities; residential mortgages and home equity loans; and credit cards, payment solutions, travel services, merchant offers, lifestyle benefits, auto loans, and leases to consumers and small businesses through bank branches, ATMs, and digital and telephone banking. It also provides investment banking, market-making, financing, custody, and securities products and services; corporate strategy and structure advisory, equity and debt market capital-raising, and loan origination and syndication services; cash and derivative instruments, risk management solutions, prime brokerage, clearing, and research; and fund services, liquidity and trading services, and data solutions products for large corporations, financial institutions, merchants, start-ups, small and midsized companies, local governments, municipalities, nonprofits, and commercial real estate clients. In addition, the company offers multi-asset investment management solutions in equities, fixed income, alternatives, and money market funds to institutional clients and retail investors; retirement products and services, estate planning, lending, deposits, and investment management products to high-net-worth clients; and financial transaction processing. JPMorgan Chase & Co. was founded in 1799 and is headquartered in New York, New York. Source: EODHD Key Stats

This week's Stock Spotlight is NYSE-listed Wells Fargo & Company. About Wells Fargo & Company. Wells Fargo & Company, a financial services company, provides diversified banking, investment, mortgage, and consumer and commercial finance products and services in the United States and internationally. It operates through four segments: Consumer Banking and Lending; Commercial Banking; Corporate and Investment Banking; and Wealth and Investment Management. The company's financial products and services includes checking and savings accounts, and credit and debit cards, as well as home, auto, personal, and small business lending services. It also provides personalized wealth management, brokerage, financial planning, lending, private banking, trust and fiduciary products and services; and financial solutions to private, family owned and public companies through products and services including banking and credit products across multiple industry sectors and municipalities, secured lending and lease products, and treasury management. In addition, it offers a suite of capital markets, banking, and financial products and services, such as corporate banking, investment banking, treasury management, commercial real estate lending and servicing, equity, and fixed income solutions, as well as sales, trading, and research capabilities services to corporate, commercial real estate, government, and institutional clients. Wells Fargo & Company was founded in 1852 and is headquartered in San Francisco, California. Source: EODHD Key Stats

This week's Stock Spotlight is NYSE-listed Bank of America Corp. About Bank of America Corp. Bank of America Corporation, through its subsidiaries, provides various financial products and services for individual consumers, small and middle-market businesses, institutional investors, large corporations, and governments worldwide. It operates through four segments: Consumer Banking, Global Wealth & Investment Management (GWIM), Global Banking, and Global Markets. The Consumer Banking segment offers traditional and money market savings accounts, certificates of deposit and IRAs, checking accounts, and investment accounts and products; credit and debit cards; residential mortgages and home equity loans; and direct and indirect loans. The GWIM segment provides investment management, brokerage, banking, and trust and retirement products and services; wealth management solutions; and customized solutions, including specialty asset management services. The Global Banking segment offers lending products and services, including commercial loans, leases, commitment facilities, trade finance, and commercial real estate and asset-based lending; treasury solutions, and underwriting and advisory services. The Global Markets segment provides market-making, financing, securities clearing, settlement, and custody services; securities and derivative products; and risk management products using interest rate, equity, credit, currency and commodity derivatives, foreign exchange, fixed-income, and mortgage-related products. Bank of America Corporation was founded in 1784 and is based in Charlotte, North Carolina. Source: EODHD Key Stats

This week's Stock Spotlight is NYSE-listed Citigroup Inc. About Citigroup Inc. Citigroup Inc., a diversified financial service holding company, provides various financial products and services to consumers, corporations, governments, and institutions. It operates through five segments: Services, Markets, Banking, U.S. Personal Banking, and Wealth. The Services segment includes treasury and trade solutions, which provides cash management, trade, and working capital solutions to multinational corporations, financial institutions, and public sector organizations; and securities services, such as cross-border support for clients, local market expertise, post-trade technologies, data solutions, and various securities services solutions. The Markets segment offers sales and trading services for equities, foreign exchange, rates, spread products, and commodities to corporate, institutional, and public sector clients; and market-making services, including asset classes, risk management solutions, financing, and prime brokerage. The Banking segment includes investment banking services comprising equity and debt capital markets-related strategic financing solutions; advisory services related to mergers and acquisitions, divestitures, restructurings, and corporate defense activities; and corporate lending consists of corporate and commercial banking. The U.S. Personal Banking segment provides proprietary and co-branded card portfolios; and traditional banking services to retail and small business customers. The Wealth segment offers financial services to high-net-worth clients through banking, lending, mortgages, investment, custody, and trust product offerings; professional industries, including law firms, consulting groups, accounting, and asset management; and affluent and high net worth clients. The company operates in North America, the United Kingdom, Japan, North and South Asia, Australia, Europe, the Middle East, and Africa. Citigroup Inc. was founded in 1812 and is headquartered in New York, New York. Source: EODHD Key Stats

AI is driving unprecedented demand for data centres. Discover how the infrastructure powering AI is creating opportunities across energy, property and technology.

About Capstone Copper Corp. Capstone Copper Corp., a copper mining company, mines, explores for, and develops mineral properties in the United States, Chile, and Mexico. The company primarily explores copper, silver, gold, molybdenum, zinc, iron, cobalt, and other base metals. Capstone Copper Corp. is headquartered in Vancouver, Canada. Source: EODHD Key Stats