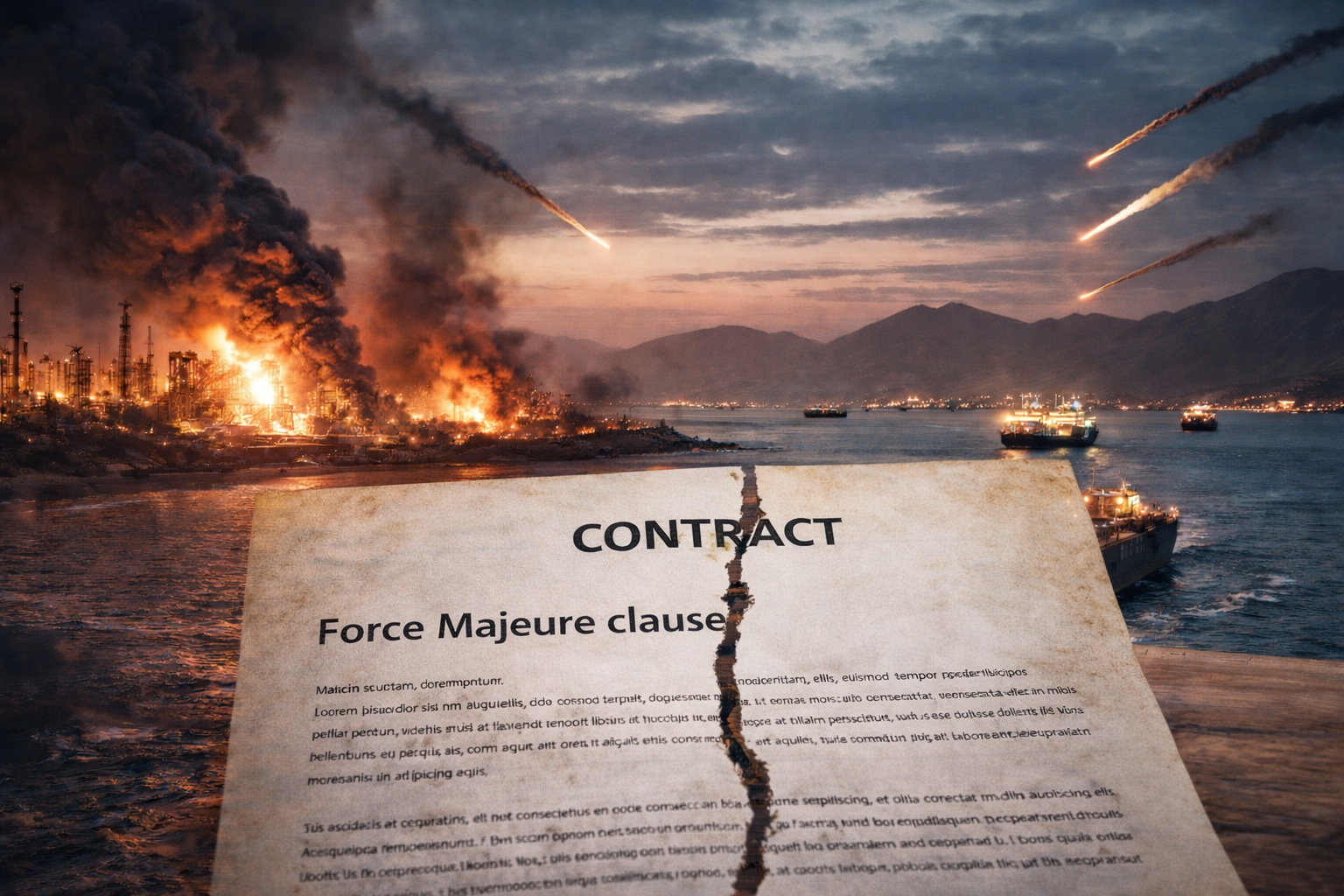

Force Majeure: The Hidden Risk Amplifying the Global Oil Crisis

Oil markets are accustomed to disruption. Geopolitical tensions, OPEC production decisions, and infrastructure outages have long shaped supply and pricing. In most cases, markets adjust. Prices reprice, inventories are drawn down, and supply eventually finds an alternative path.

The current environment is materially different. The disruption across the Persian Gulf, centred on the closure of the Strait of Hormuz, has not simply tightened supply. It has removed it. Roughly 20% of global oil and liquefied natural gas flows through this chokepoint. With transit restricted, producers with crude ready to export have been unable to move it. Storage capacity has filled, production has been shut in, and supply has been taken off the market entirely.

At the centre of this shift is a concept often overlooked outside legal and contract circles: force majeure. What is typically seen as a contractual clause has become a key mechanism through which supply shocks are transmitted into markets. Recent declarations across the Gulf have formalised the disruption, confirming that the interruption is neither temporary nor easily resolved by any single party.

From a portfolio perspective, the distinction is critical. A disruption that tightens supply can be absorbed and priced over time. A disruption that removes supply, with uncertain duration, creates a different form of volatility. Force majeure does not delay supply. It suspends it. In doing so, it converts geopolitical conflict into immediate and measurable market impact.

What Force Majeure Means in Practice

Force majeure is a standard clause in commercial contracts that allows a party to suspend or be excused from its obligations when an extraordinary event beyond its control makes performance impossible. The term, derived from French meaning “superior force”, is embedded across commodity contracts, shipping agreements, and infrastructure arrangements throughout the global energy market.

In energy markets, this typically applies to producers, exporters, and transport operators who are unable to deliver oil due to external events. Common triggers include war, sanctions, infrastructure damage, and shipping disruptions. In the current environment, the combination of military conflict, restricted shipping routes, and direct threats to export infrastructure has created conditions where these clauses are being actively invoked.

The key distinction is that force majeure is not a delay. It is a legal suspension of delivery obligations, often with immediate effect. When invoked, contracted supply does not arrive late. It does not arrive at all. Buyers expecting delivery must secure alternative supply on the spot market, often at significantly higher prices, or absorb the shortfall. Supply does not decline gradually. It stops, and the timing of its return is often uncertain.

This binary outcome is what makes force majeure particularly disruptive. Markets are forced to reprice rapidly as expected supply disappears and replacement demand emerges. The uncertainty is compounded by the legal complexity of each declaration. Force majeure must meet strict contractual definitions and demonstrate that performance is genuinely prevented. Many recent declarations are likely to face prolonged legal scrutiny, adding another layer of uncertainty to already volatile markets.

The Cascade: From Qatar to Iraq

The force majeure declarations of March 2026 did not occur in isolation. They unfolded in sequence, each reinforcing and amplifying the market signal of the last.

QatarEnergy was among the first to act, declaring force majeure on all LNG exports following the effective closure of the Strait of Hormuz. Strikes on the Ras Laffan complex damaged key infrastructure, removing an estimated 12.8 million tonnes of annual LNG capacity. With tanker access restricted, liquefaction operations were halted entirely.

The disruption quickly spread. Kuwait reduced production to domestic demand levels, while Bahrain suspended refining operations as supply chains tightened. Each development reinforced the severity of the disruption and the inability of producers to maintain export flows.

The most significant escalation came from Iraq. Force majeure was declared across oilfields operated by foreign partners after export routes became inaccessible. Despite having crude available, the inability to load shipments forced a shutdown of production as storage reached capacity. Foreign operators were not entitled to compensation under existing contract terms, highlighting the financial implications of the declaration. For Iraq, where crude exports account for more than 90% of government revenue, the decision reflected both operational necessity and fiscal stress.

The ripple effects extended beyond producers. Energy supply reallocations and downstream disruptions reinforced a single conclusion. The disruption was intensifying, not resolving, and contractual frameworks were being tested under extreme conditions.

From Clause to Crisis: How Force Majeure Amplifies Oil Shocks

The transmission from force majeure declaration to market impact follows a clear sequence. A physical disruption occurs, producers suspend contractual obligations, and contracted supply is removed from the market. Buyers enter the spot market simultaneously, competing for limited supply and driving prices higher. Inventories are drawn down as consumption outpaces replenishment.

This sequence unfolded rapidly. Brent crude moved above USD 100 per barrel and reached USD 126 at its peak. The effects extended beyond pricing.

Shipping and insurance costs rose sharply as war risk premiums increased before commercial traffic slowed significantly. Refiners in Asia and Europe faced feedstock shortages as contracted cargoes failed to arrive, disrupting downstream operations.

The impact was broader than energy. The Strait of Hormuz is a key route for fertiliser inputs, aluminium, and food imports. Disruptions to these flows placed pressure on global supply chains, contributing to rising input costs across multiple sectors.

For investors, the transmission is direct. Supply disruptions in energy markets flow through to transport, production, and agriculture, reinforcing inflationary pressure across the global economy.

Why Markets Struggle to Price It

Force majeure introduces a form of risk that is difficult to price. Unlike gradual shifts in supply or demand, it is binary. Supply is either available or it is not.

The duration of disruption is uncertain. Outcomes depend on geopolitical developments, infrastructure repair, and policy response, creating a wide range of scenarios. This uncertainty complicates forward pricing and increases volatility.

Legal complexity adds another layer. The validity of force majeure declarations can be contested, and disputes may take years to resolve. This extends uncertainty beyond the immediate disruption.

Markets are therefore driven not only by current fundamentals but by the range of possible outcomes. Pricing reflects uncertainty as much as it reflects supply and demand.

Winners, Losers and Market Implications

The impact of force majeure is uneven. Energy producers with supply outside the affected region benefit from higher realised prices and improved cash flow. LNG exporters in Australia and the United States are well positioned as global supply tightens, with ASX-listed producers benefiting from repricing.

Sectors with high fuel exposure face immediate pressure. Airlines, transport operators, and energy-intensive industries experience rising input costs and margin compression. Import-dependent economies face both inflation and growth headwinds.

Australia occupies a dual position. As an LNG exporter, it benefits from higher global prices. As an importer of approximately 90% of its liquid fuel, it remains exposed to supply disruption. This divergence supports energy equities while placing pressure on the broader market.

At the macro level, force majeure-driven supply shocks reinforce inflation. Higher energy prices flow through to transport, production, and consumer goods, limiting the ability of central banks to ease policy. With the Reserve Bank of Australia at 4.10% and global central banks maintaining restrictive settings, the outlook remains skewed toward a higher-for-longer rate environment.

Portfolio Construction: Rethinking Diversification in a Supply Shock Environment

Force majeure highlights a fundamental limitation of traditional diversification. Most allocation frameworks are built around demand-driven cycles where asset correlations behave predictably. Supply shocks driven by geopolitical conflict operate differently. They are sudden, binary, and often cause assets that are expected to diversify risk to move in the same direction, particularly when inflation is the dominant force.

These shocks are also largely outside the reach of policy response. Central banks cannot address supply constraints directly, and fiscal measures tend to focus on managing demand rather than restoring disrupted supply. This creates an environment where inflation persists and volatility increases, reducing the effectiveness of traditional defensive assets.

This reinforces the need to focus on underlying risk drivers rather than asset labels. Energy and commodity exposure can provide a hedge against supply-driven inflation, though these positions are cyclical and require active management. Real assets and infrastructure benefit from the repricing of physical supply chains, while short-duration fixed income helps reduce sensitivity to rising yields. Currency exposure also plays a role, with a stronger US dollar often supporting returns for unhedged international allocations.

Flexibility becomes critical. Static allocation frameworks are less effective when correlations shift and shocks are externally driven. Maintaining liquidity, adjusting positioning as conditions evolve, and recognising that supply shocks are inherently harder to hedge than demand shocks are central to navigating this environment.

Conclusion: A Legal Clause Driving Market Outcomes

Force majeure is no longer confined to legal language within commodity contracts. In 2026, it has emerged as a key mechanism shaping global energy markets. Declarations across the Gulf, from LNG shutdowns in Qatar to production halts in Iraq, have confirmed that supply is not simply disrupted but removed, often with uncertain duration and broad market consequences.

Its relevance extends beyond the current crisis. Force majeure risk is likely to become more prominent as geopolitical fragmentation deepens, energy infrastructure becomes increasingly exposed in conflict, and critical supply routes remain vulnerable. The Strait of Hormuz is one example, but similar risks exist across multiple trade corridors and commodities.

The investors best positioned for this environment are those who recognise that some of the most consequential market risks are sudden, binary, and driven by events that fall outside traditional economic models. Force majeure is the legal expression of that reality. Understanding it is no longer optional, it is now part of the market vocabulary.

Whether you're reviewing your asset allocation, reassessing duration exposure, or exploring diversification strategies suited to the current environment, we encourage you to

speak with an adviser for strategic guidance aligned to current market dynamics.

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

AI spending is accelerating in 2026. Learn how to read AI earnings, spot overhyped stocks and find companies converting AI investment into real profit.

Wall Street posted its strongest quarter since 2020. Discover what's driving the rally, why the US outperformed the ASX, and what it means for Australian investors.

About Oracle Corporation Oracle Corporation offers products and services that build, run and support enterprise information technology frameworks worldwide. Its Oracle cloud software as a service offering includes various cloud software applications, including Oracle Fusion cloud enterprise resource planning ERP, Oracle Fusion cloud enterprise performance management EPM, Oracle Fusion cloud supply chain and manufacturing management SCM, Oracle Fusion cloud human capital management HCM, and NetSuite applications suite, Oracle Health applications, as well as Oracle Fusion Sales, Service, and Marketing. The company also offers cloud-based industry solutions for various industries; Oracle cloud license and on-premise license; and Oracle license support services. In addition, it provides cloud and license business' infrastructure technologies, such as the Oracle Database and MySQL Database; Java, a software development language; and middleware, including development tools and others. The company's cloud and license business' infrastructure technologies also comprise cloud-based compute, storage, and networking capabilities; and Oracle autonomous database, as well as AI, Internet-of-Things, machine learning, digital assistant, and blockchain. Further, it provides hardware products and other hardware-related software offerings, including Oracle engineered systems, enterprise servers, storage solutions, industry-specific hardware, virtualization software, operating systems, management software, and related hardware support services, and consulting and advanced customer services. It markets and sells its cloud, license, hardware, support, and services offerings directly to businesses in various industries, government agencies, and educational institutions, as well as through indirect channels. Oracle Corporation has a strategic alliance with Metron, Inc. The company was founded in 1977 and is headquartered in Austin, Texas. Source: EODHD Key Stats

About HDFC Bank Limited HDFC Bank Limited provides banking and financial products and services to individuals and businesses in India, Bahrain, Hong Kong, Singapore, and Dubai. The company operates through Treasury, Retail Banking, Wholesale Banking, Other Banking Business, Insurance Business, and Other segments. It offers savings, salary, current, rural, public provident fund, pension, and demat accounts; fixed and recurring deposits; and safe deposit lockers, as well as offshore accounts and deposits, and overdrafts against fixed deposits. The company also provides personal, home, car, two-wheeler, business, doctor, educational, gold, consumer, and rural loans; loans against properties, securities, mutual funds, rental receivables, and assets; loans for professionals; government sponsored programs; and loans on credit card, as well as working capital and commercial/construction equipment finance, healthcare/medical equipment, commercial vehicle finance, dealer finance, and term loans. In addition, it offers credit, debit, prepaid, forex, and kisan gold cards; payment and collection, export, import, remittance, bank guarantee, letter of credit, trade, hedging, and merchant and cash management services; and insurance and investment products. Further, the company provides short term finance, bill discounting, structured finance, export credit, loan repayment, custodial, and documents collection services; online, mobile, and phone banking services; unified payment interface, immediate payment, national electronic funds transfer, and real time gross settlement services; channel financing, vendor financing, reimbursement account, money market, derivatives, employee trusts, cash surplus corporates, tax payment, and bankers to rights/public issue services; and financial solutions for supply chain partners and agricultural customers. It operates branches and automated teller machines in various cities/towns. The company was incorporated in 1994 and is headquartered in Mumbai, India. Source: EODHD Key Stats

About Woodside Energy Group Woodside Energy Group Ltd engages in the exploration, evaluation, development, production, marketing, and sale of hydrocarbons in the Asia Pacific, Africa, the Americas, and the Europe. It produces liquefied natural gas, pipeline gas, crude oil and condensate, and natural gas liquids. The company holds interests in the Pluto LNG, North West Shelf, Wheatstone and Julimar-Brunello, Bass Strait, Ngujima-Yin FPSO, Okha FPSO, Pyrenees FPSO, Macedon, Shenzi, Mad dog, Greater Angostura, as well as Scarborough, Sangomar, Trion, Calypso, Browse, Liard, Ruby, Sangomar, Atlantis, Woodside Solar opportunity, and Sunrise and Troubadour. It is also involved in the development of new energy products and lower-carbon services. The company was formerly known as Woodside Petroleum Ltd and changed its name to Woodside Energy Group Ltd in May 2022. Woodside Energy Group Ltd was founded in 1954 and is headquartered in Perth, Australia. Source: EODHD Key Stats

About Metcash Ltd Metcash Limited operates as a wholesale and distribution company in Australia. The company operates through Food, Liquor, and Hardware segments. Its Food segment distributes a range of products and services to independent supermarket, convenience retail outlets, and food service customers. The Liquor segment engages in the distribution of liquor products to independent retail outlets and hotels. Its Hardware segment distributes hardware products to independent retail outlets; and operates company owned retail stores. The company sells its products under the IGA, Foodland, Mitre 10, Home Hardware, Total Tools, Cellarbrations, IGA Liquor, and the Bottle-O brand names. Metcash Limited was founded in 1927 and is based in Macquarie Park, Australia. Source: EODHD Key Stats

SMSFs can no longer borrow to buy residential property. A clear look at what changed, the 45-day window to act, and what it means for your retirement strategy.

What made RPMGlobal (ASX: RUL) worth $1.1B to Caterpillar? Explore the SaaS transition, the 5-year hold & the long-term ASX investing lessons from this deal.

About Alibaba Group Holding Ltd Alibaba Group Holding Limited, through its subsidiaries, provides technology infrastructure and marketing reach to help merchants, brands, retailers, and other businesses in the People's Republic of China and internationally. It operates through the Alibaba China E-Commerce Group, Alibaba International Digital Commerce Group, Cloud Intelligence Group, and All Others segments. The Alibaba China E-commerce Group segment operates Taobao and Tmall, which are digital retail platforms; Taobao Instant Commerce, a local services and on-demand delivery platform; 1688.com, a domestic wholesale marketplace; and Xianyu, a consumer-to-consumer community and marketplace for idle goods. Its Alibaba International Digital Commerce Group segment includes AliExpress, a global e-commerce platform; Trendyol, an e-commerce platform in Turkey; Lazada, an e-commerce platform in Southeast Asia; Daraz, an e-commerce platform in South Asia, primarily in Pakistan and Bangladesh; and Alibaba.com, an integrated international online wholesale marketplace. The Cloud Intelligence Group segment offers a suite of cloud services based on infrastructure-as-a-service, platform-as-a-service, and model-as-a-service. Its All Others segment comprises Amap, a provider of mobile digital maps, navigation, and real-time traffic information in China; Cainiao, which provides logistics solutions; Youku, an online long-form video platform in China; Freshippo, a retail platform for groceries and fresh goods; and Alibaba Health, a pharmaceutical and healthcare services platform. Alibaba Group Holding Limited was incorporated in 1999 and is based in Hangzhou, China. Source: EODHD Key Stats

About Technology One Ltd Technology One Limited engages in the development, marketing, sale, implementation, and support of integrated enterprise business software solutions in Australia and internationally. It operates through Software and Consulting segments. The company offers various business software solutions, including business analytics, app builder, corporate performance management, curriculum, DxP local government, DxP Student, DxP Essentials, enterprise asset management, enterprise budgeting, enterprise cash receipting, enterprise content management, financials, human resources and payroll, performance planning, property and rating, spatial, student management, timetabling and scheduling, and supply chain management. It serves local government, education, government, health and community services, asset and project intensive, and financial services and corporate organizations. Technology One Limited was incorporated in 1983 and is headquartered in Fortitude Valley, Australia. Source: EODHD Key Stats