From Ceasefire to Blockade in 72 Hours: What Actually Happened?

In geopolitics, sentiment can turn quickly when underlying tensions are unresolved. The collapse of recent United States and Iran negotiations was not a sudden reversal, but the inevitable outcome of positions that were never aligned despite a brief window of optimism.

On 8 April, markets rallied on the announcement of a two-week ceasefire. Oil fell 16% in its largest one-day decline since the pandemic, the ASX rose 2.6%, and Qantas Airways Limited gained 9% as investors priced in easing risk. Within seventy-two hours, that optimism reversed. Talks collapsed after 21 hours in Islamabad, the United States imposed a naval blockade on Iranian ports, and markets repriced sharply. Oil moved back above US$104 per barrel, the Australian dollar weakened, and the Reserve Bank of Australia acknowledged rising stagflation risk.

This was not a gradual deterioration but a rapid shift from diplomacy to enforcement. Markets had priced in peace, but what existed was only a temporary pause with no shared end state. The failure of talks did not create risk, it revealed it. The blockade represents a decisive escalation, but also a broader signal that economic coercion is once again a primary tool of statecraft.

What the Talks Were Trying to Achieve

Before examining why the Islamabad talks failed, it is necessary to understand the scale of what they were attempting to deliver. The negotiations aimed to establish a verified framework to constrain Iran’s nuclear programme in exchange for sanctions relief, effectively a successor to the agreement abandoned in 2018. Attempting to reach such an outcome during an active conflict, within a compressed timeframe, left limited room for compromise.

The United States entered with clear non-negotiable demands. These included verifiable limits on uranium enrichment, dismantling advanced centrifuge infrastructure, removal of highly enriched uranium stockpiles, and cessation of funding for regional militant groups such as Hezbollah. Iran’s position moved in the opposite direction. Tehran sought full sanctions relief, recognition of its right to enrich uranium, security guarantees against future military action, compensation for war-related damage, and recognition of its influence over the Strait of Hormuz.

Despite these differences, expectations remained cautiously constructive. Both sides faced genuine pressure. Iran’s oil revenues had been disrupted, while the United States was managing elevated fuel prices and domestic political sensitivity. Pakistan’s role as a neutral intermediary enabled both delegations to engage. The incentives to negotiate were present, but the underlying positions remained structurally incompatible.

The Breakdown: Why Talks Collapsed

The collapse of the talks was not a last-minute failure. The structural conditions required for agreement were absent from the outset, and the 21 hours of discussions confirmed this reality.

Three fault lines defined the negotiations. The first was a deep trust deficit. Iran’s position was shaped by the 2018 withdrawal from the original agreement and the reimposition of sanctions despite prior compliance. From Tehran’s perspective, any new agreement carried a high risk of being abandoned. The United States viewed Iran’s continued enrichment activity as evidence of bad faith. Both positions were grounded in recent history, making compromise difficult.

The second fault line was the absence of a credible enforcement framework. The United States required verifiable nuclear concessions before offering sanctions relief. Iran demanded sanctions relief as a precondition for any concessions. Both positions are internally consistent but incompatible. Without a trusted third-party verification mechanism, sequencing could not be resolved.

The third was a mismatch in timelines and strategic priorities. The United States sought rapid, measurable outcomes. Iran’s position reflected a longer-term strategic approach in which its nuclear programme is tied to sovereignty and long-term security. These perspectives could not be reconciled within a compressed negotiation window.

The breakdown reflected structural incompatibility rather than negotiation failure. The speed of escalation that followed highlighted how little room there was for delay.

The Pivot: Why the United States Chose a Naval Blockade

With diplomacy exhausted, the United States faced limited options. Accepting a nuclear-capable Iran with influence over a critical energy corridor was not politically viable. Resuming direct military strikes carried significant escalation and diplomatic risks. Economic pressure emerged as the most viable alternative, targeting Iran’s primary revenue source through oil exports.

Iran’s oil sector generates approximately USD45 billion annually, or around 13% of GDP, with exports near 1.85 million barrels per day. Disrupting this flow applies direct economic pressure without the costs associated with military engagement. A naval blockade allows enforcement to take effect immediately through interception and rerouting of vessels.

The blockade offers three advantages. It delivers immediate impact, carries lower political cost than military strikes, and provides flexibility. Enforcement can be scaled depending on Iran’s response, maintaining leverage.

Its scope is also deliberate. The blockade targets Iranian ports while allowing freedom of navigation through the Strait of Hormuz for non-Iranian traffic. This approach aims to restrict Iranian exports without fully disrupting global energy flows. Its effectiveness depends on the compliance of third-party actors such as China, India and Russia, which remain the key variable in determining outcomes.

The First 72 Hours: Theory Becoming Real-World Disruption

The events following the collapse illustrate how quickly geopolitical decisions translate into economic outcomes. On 12 April, negotiations ended with conflicting statements and oil moved higher in after-hours trading.

Within 48 hours, the blockade was implemented. Shipping routes were adjusted, insurance costs increased, and vessels carrying Iranian crude faced interception risk. Risk-sensitive currencies weakened, oil prices rose, and Asia-Pacific equities declined.

By 14 April, the effects had extended into corporate earnings and sentiment. Qantas Airways Limited warned of up to AUD800 million in additional fuel costs. Westpac Banking Corporation and National Australia Bank flagged deteriorating credit conditions. Consumer sentiment declined sharply. The Reserve Bank of Australia warned of a potential stagflationary shock.

These developments emerged within forty-eight hours of the blockade, demonstrating how quickly geopolitical risk now feeds through markets and the real economy.

Market and Economic Implications: From Global Shock to Domestic Transmission

At the global level, the brief removal of the risk premium during the ceasefire has fully reversed. The blockade directly threatens Iran’s oil exports, which were running at approximately 1.7 million barrels per day, tightening already constrained physical markets. Even where actual supply disruption remains contained, the reintroduction of uncertainty has been sufficient to drive price volatility. At the same time, freight and insurance markets are repricing risk across key shipping routes, with disruptions likely to persist well beyond any near-term diplomatic resolution. The situation also introduces new geopolitical flashpoints, particularly around enforcement, including the potential targeting of third-party vessels, which could materially escalate tensions.

These global pressures are now transmitting directly into the Australian economy through multiple channels. The most immediate is fuel and inflation. Australia imports close to 90% of its refined fuel, making it highly exposed to sustained increases in oil prices. The cost pressures flagged by Qantas Airways Limited are indicative of a broader dynamic affecting transport, logistics and manufacturing. Persistently elevated oil prices are likely to flow through to headline inflation, complicating the policy outlook for the Reserve Bank of Australia.

This feeds directly into interest rate expectations. Markets are increasingly pricing further tightening as the central bank balances rising inflation against slowing growth. The use of stagflationary language by policymakers signals a willingness to prioritise inflation control, even at the expense of economic momentum. At the corporate level, early warnings from institutions such as Westpac Banking Corporation and National Australia Bank point to rising credit stress and deteriorating business conditions as higher input costs and borrowing rates converge.

Equity markets are already reflecting these shifts. The rotation observed during the ceasefire period has reversed, with energy producers benefiting from higher prices while banks and consumer-facing sectors come under renewed pressure. More broadly, the environment reinforces a defensive positioning bias, with dispersion increasing across sectors as investors respond to a combination of higher costs, tighter financial conditions and elevated geopolitical risk.

Conclusion: A Shift from Hope to Reality

The pace of this escalation is the defining feature. Markets moved from a ceasefire-driven rally to pricing an active naval blockade within seventy-two hours, while policymakers shifted from cautious optimism to openly discussing stagflation within the same week. What changed was not the underlying reality, but the market’s understanding of it. Diplomacy created hope, but the structural differences between the United States and Iran meant a durable agreement was never in place.

The blockade is now the central fact shaping global energy markets and will remain so until one of three outcomes emerges: a credible return to negotiations, economic pressure forcing Iranian concessions, or escalation into a broader conflict. In the meantime, the reintroduction of a sustained geopolitical risk premium is already feeding through commodities, trade flows, monetary policy expectations and corporate earnings.

For Australian investors, the implication is clear. The question is no longer whether this matters, but whether it is being understood with sufficient clarity to inform deliberate decisions. With CPI data, an election cycle and the next Reserve Bank of Australia meeting all imminent, the coming weeks represent a critical window. This is not simply another news cycle. It is a live macro shock, and how it is interpreted will directly shape outcomes across portfolios, policy and the broader economy.

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

This week's Stock Spotlight is NYSE-listed Wells Fargo & Company. About Wells Fargo & Company. Wells Fargo & Company, a financial services company, provides diversified banking, investment, mortgage, and consumer and commercial finance products and services in the United States and internationally. It operates through four segments: Consumer Banking and Lending; Commercial Banking; Corporate and Investment Banking; and Wealth and Investment Management. The company's financial products and services includes checking and savings accounts, and credit and debit cards, as well as home, auto, personal, and small business lending services. It also provides personalized wealth management, brokerage, financial planning, lending, private banking, trust and fiduciary products and services; and financial solutions to private, family owned and public companies through products and services including banking and credit products across multiple industry sectors and municipalities, secured lending and lease products, and treasury management. In addition, it offers a suite of capital markets, banking, and financial products and services, such as corporate banking, investment banking, treasury management, commercial real estate lending and servicing, equity, and fixed income solutions, as well as sales, trading, and research capabilities services to corporate, commercial real estate, government, and institutional clients. Wells Fargo & Company was founded in 1852 and is headquartered in San Francisco, California. Source: EODHD Key Stats

This week's Stock Spotlight is NYSE-listed Bank of America Corp. About Bank of America Corp. Bank of America Corporation, through its subsidiaries, provides various financial products and services for individual consumers, small and middle-market businesses, institutional investors, large corporations, and governments worldwide. It operates through four segments: Consumer Banking, Global Wealth & Investment Management (GWIM), Global Banking, and Global Markets. The Consumer Banking segment offers traditional and money market savings accounts, certificates of deposit and IRAs, checking accounts, and investment accounts and products; credit and debit cards; residential mortgages and home equity loans; and direct and indirect loans. The GWIM segment provides investment management, brokerage, banking, and trust and retirement products and services; wealth management solutions; and customized solutions, including specialty asset management services. The Global Banking segment offers lending products and services, including commercial loans, leases, commitment facilities, trade finance, and commercial real estate and asset-based lending; treasury solutions, and underwriting and advisory services. The Global Markets segment provides market-making, financing, securities clearing, settlement, and custody services; securities and derivative products; and risk management products using interest rate, equity, credit, currency and commodity derivatives, foreign exchange, fixed-income, and mortgage-related products. Bank of America Corporation was founded in 1784 and is based in Charlotte, North Carolina. Source: EODHD Key Stats

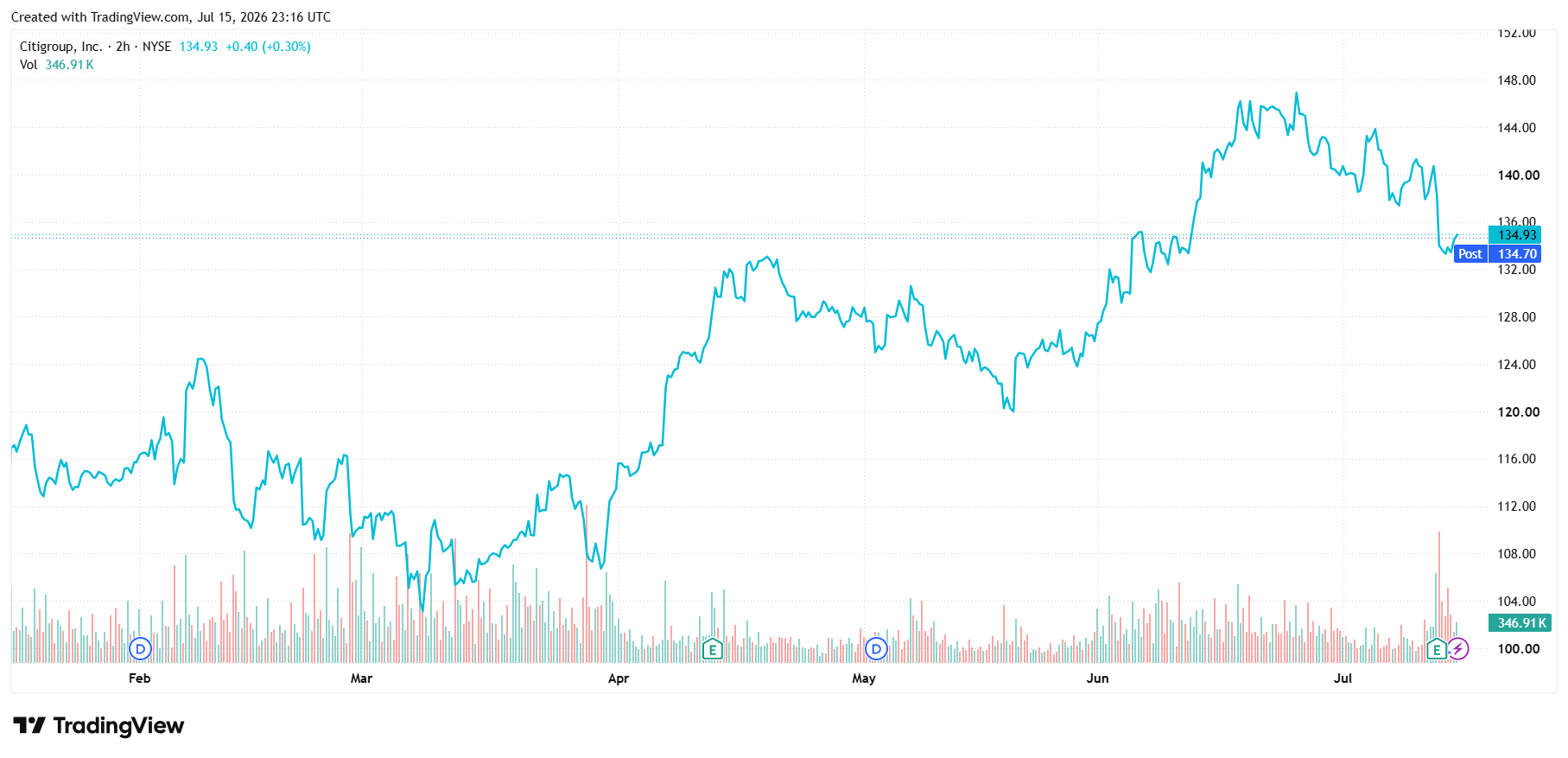

This week's Stock Spotlight is NYSE-listed Citigroup Inc. About Citigroup Inc. Citigroup Inc., a diversified financial service holding company, provides various financial products and services to consumers, corporations, governments, and institutions. It operates through five segments: Services, Markets, Banking, U.S. Personal Banking, and Wealth. The Services segment includes treasury and trade solutions, which provides cash management, trade, and working capital solutions to multinational corporations, financial institutions, and public sector organizations; and securities services, such as cross-border support for clients, local market expertise, post-trade technologies, data solutions, and various securities services solutions. The Markets segment offers sales and trading services for equities, foreign exchange, rates, spread products, and commodities to corporate, institutional, and public sector clients; and market-making services, including asset classes, risk management solutions, financing, and prime brokerage. The Banking segment includes investment banking services comprising equity and debt capital markets-related strategic financing solutions; advisory services related to mergers and acquisitions, divestitures, restructurings, and corporate defense activities; and corporate lending consists of corporate and commercial banking. The U.S. Personal Banking segment provides proprietary and co-branded card portfolios; and traditional banking services to retail and small business customers. The Wealth segment offers financial services to high-net-worth clients through banking, lending, mortgages, investment, custody, and trust product offerings; professional industries, including law firms, consulting groups, accounting, and asset management; and affluent and high net worth clients. The company operates in North America, the United Kingdom, Japan, North and South Asia, Australia, Europe, the Middle East, and Africa. Citigroup Inc. was founded in 1812 and is headquartered in New York, New York. Source: EODHD Key Stats

AI is driving unprecedented demand for data centres. Discover how the infrastructure powering AI is creating opportunities across energy, property and technology.

About Capstone Copper Corp. Capstone Copper Corp., a copper mining company, mines, explores for, and develops mineral properties in the United States, Chile, and Mexico. The company primarily explores copper, silver, gold, molybdenum, zinc, iron, cobalt, and other base metals. Capstone Copper Corp. is headquartered in Vancouver, Canada. Source: EODHD Key Stats

About Qualcomm Inc. QUALCOMM Incorporated engages in the development and commercialization of foundational technologies for the wireless industry worldwide. It operates through three segments: Qualcomm CDMA Technologies (QCT); Qualcomm Technology Licensing (QTL); and Qualcomm Strategic Initiatives (QSI). The QCT segment develops and supplies integrated circuits and system software with connectivity and computing technologies for use in mobile devices; automotive systems for connectivity, digital cockpit, and ADAS/AD; and IoT, including consumer electronic devices, industrial devices, and edge networking products. The QTL segment grants licenses or provides rights to use portions of its intellectual property portfolio, which include various patent rights useful in the manufacture and sale of wireless products comprising products implementing LTE, and/or OFDMA-based 5G products and derivatives; to use cellular standard-essential patents, including 3G, 4G and 5G for cellular devices. The QSI segment invests in early-stage companies in various industries, including 5G, artificial intelligence, automotive, consumer, enterprise, cloud, IoT, and extended reality, and investments, including non-marketable equity securities and, to a lesser extent, marketable equity securities, and convertible debt instruments. It also provides development, and other services and sells related products to the United States government agencies and their contractors. In addition, the company is also involved in Qualcomm government technologies and data center businesses. Further, it provides security and intelligence services for unmanaged networks through software-based network security solutions. QUALCOMM Incorporated was incorporated in 1985 and is headquartered in San Diego, California. Source: EODHD Key Stats

AI spending is accelerating in 2026. Learn how to read AI earnings, spot overhyped stocks and find companies converting AI investment into real profit.

Wall Street posted its strongest quarter since 2020. Discover what's driving the rally, why the US outperformed the ASX, and what it means for Australian investors.

About Oracle Corporation Oracle Corporation offers products and services that build, run and support enterprise information technology frameworks worldwide. Its Oracle cloud software as a service offering includes various cloud software applications, including Oracle Fusion cloud enterprise resource planning ERP, Oracle Fusion cloud enterprise performance management EPM, Oracle Fusion cloud supply chain and manufacturing management SCM, Oracle Fusion cloud human capital management HCM, and NetSuite applications suite, Oracle Health applications, as well as Oracle Fusion Sales, Service, and Marketing. The company also offers cloud-based industry solutions for various industries; Oracle cloud license and on-premise license; and Oracle license support services. In addition, it provides cloud and license business' infrastructure technologies, such as the Oracle Database and MySQL Database; Java, a software development language; and middleware, including development tools and others. The company's cloud and license business' infrastructure technologies also comprise cloud-based compute, storage, and networking capabilities; and Oracle autonomous database, as well as AI, Internet-of-Things, machine learning, digital assistant, and blockchain. Further, it provides hardware products and other hardware-related software offerings, including Oracle engineered systems, enterprise servers, storage solutions, industry-specific hardware, virtualization software, operating systems, management software, and related hardware support services, and consulting and advanced customer services. It markets and sells its cloud, license, hardware, support, and services offerings directly to businesses in various industries, government agencies, and educational institutions, as well as through indirect channels. Oracle Corporation has a strategic alliance with Metron, Inc. The company was founded in 1977 and is headquartered in Austin, Texas. Source: EODHD Key Stats

About HDFC Bank Limited HDFC Bank Limited provides banking and financial products and services to individuals and businesses in India, Bahrain, Hong Kong, Singapore, and Dubai. The company operates through Treasury, Retail Banking, Wholesale Banking, Other Banking Business, Insurance Business, and Other segments. It offers savings, salary, current, rural, public provident fund, pension, and demat accounts; fixed and recurring deposits; and safe deposit lockers, as well as offshore accounts and deposits, and overdrafts against fixed deposits. The company also provides personal, home, car, two-wheeler, business, doctor, educational, gold, consumer, and rural loans; loans against properties, securities, mutual funds, rental receivables, and assets; loans for professionals; government sponsored programs; and loans on credit card, as well as working capital and commercial/construction equipment finance, healthcare/medical equipment, commercial vehicle finance, dealer finance, and term loans. In addition, it offers credit, debit, prepaid, forex, and kisan gold cards; payment and collection, export, import, remittance, bank guarantee, letter of credit, trade, hedging, and merchant and cash management services; and insurance and investment products. Further, the company provides short term finance, bill discounting, structured finance, export credit, loan repayment, custodial, and documents collection services; online, mobile, and phone banking services; unified payment interface, immediate payment, national electronic funds transfer, and real time gross settlement services; channel financing, vendor financing, reimbursement account, money market, derivatives, employee trusts, cash surplus corporates, tax payment, and bankers to rights/public issue services; and financial solutions for supply chain partners and agricultural customers. It operates branches and automated teller machines in various cities/towns. The company was incorporated in 1994 and is headquartered in Mumbai, India. Source: EODHD Key Stats