Global Markets in 2026: Ten Themes Investors Should Watch

In this environment, broad market momentum alone is unlikely to sustain returns. Understanding structural growth drivers, the evolving impact of artificial intelligence, and the resilience of commodity-linked markets is increasingly important. The following themes are expected to shape portfolio thinking in 2026 and help investors navigate both opportunity and risk.

Interest Rates Are Turning, But the Path Is Unclear

Central banks in the United States, Europe, and Australia are moving away from periods of sharp rate increases toward a slower path of rate reductions. Markets are pricing some rate cuts in 2026 as inflation moderates from elevated levels. The US core personal consumption expenditures price index, a key inflation measure, is expected to move toward the Federal Reserve’s 2% target through the year. This shift supports risk assets as lower rates reduce discount rates on future earnings.

Timing and magnitude of cuts remain uncertain. If inflation or wages rise unexpectedly, rate adjustments could be delayed, influencing bond yields and equity valuations. Investors should remain flexible in fixed income positioning and maintain diversified exposure to manage potential monetary policy shifts.

Inflation Is Lower, Not Gone

Headline inflation has eased significantly from the peaks seen in 2022, but underlying price pressures remain. Energy, logistics, insurance, and labour costs are still above historical averages in major economies. Core inflation measures in developed markets are expected to hover around 2.2–2.8% in 2026. For businesses, this means managing cost structures and pricing power remains important.

Investors should focus on companies that can protect or expand margins in this environment. In fixed income, real yield exposure and inflation‑linked securities may offer resilience if inflation remains above long‑run targets. In equities, sectors such as consumer staples and utilities, which often withstand cost variability, may offer relative stability.

Artificial Intelligence: From Investment Boom to Earnings Test

Artificial intelligence remains one of the dominant structural themes underpinning market performance in 2026. Investment in AI infrastructure and applications continues at an unprecedented scale, with capital expenditure on related hardware, software and data infrastructure forecast to expand meaningfully over the coming years. Independent estimates suggest global AI‑related investment could exceed several hundred billion dollars annually, contributing to corporate capital spending even as other areas remain restrained.

Despite this scale, the narrative around AI is evolving from pure optimism toward earnings discipline. Investors are increasingly focused on whether AI spending translates into measurable productivity gains and profit growth, rather than simply driving revenue growth without margin improvement. This transition is reflected in market behaviour, where AI‑linked sectors show divergence in performance based on execution and profit outcomes. Companies that can articulate clear paths from AI adoption to bottom‑line improvement are likely to attract premium valuations, while those with heavy spending and uncertain payoffs may face multiple compression. For Australian markets, this theme intersects with industrial automation, data centre infrastructure and energy demand dynamics, reinforcing the need to differentiate quality execution from thematic exposure.

Global Growth Is Fragmented

Economic performance in 2026 is uneven across regions. The United States is expected to grow at a moderate pace supported by consumption and investment, while Europe’s expansion remains constrained by structural and demographic factors. China is forecast to grow around 4.2–4.5%, below its long‑run trend but stable, while India and several Southeast Asian economies are expanding faster, driven by domestic consumption and industrial activity. Australia is projected to grow around 2.2–2.3%, supported by resilient private consumption, stabilising labour markets, and a modest rebound in investment. Overall, global GDP growth is expected to reach 2.9–3.1%, reflecting a mix of steady expansions and slower regions.

For investors, this fragmentation highlights the importance of selective exposure. Companies with diversified global revenue streams may benefit from stronger pockets of growth, while firms tied to slower regions could face headwinds. On the ASX, resource and energy companies with export exposure to China and Southeast Asia are likely to see favourable demand conditions, while domestic-facing sectors such as property and consumer discretionary may track more closely with local household and income trends. Large-cap banks and industrials with international operations may experience varying performance depending on the pace of growth in their key markets.

China Remains a Market Swing Factor

China’s economic trajectory continues to influence global markets. As a major consumer of commodities and a key part of global supply chains, changes in Chinese policy, regulation, or trade dynamics can impact asset prices globally. Although policymakers are supporting growth with targeted measures, domestic demand remains subdued in areas such as property and retail.

Investors should view China not merely as a growth engine but as a critical determinant of global commodity demand and regional market sentiment. For Australian markets in particular, Chinese activity influences demand for iron ore, energy and industrial metals, with direct implications for ASX materials and energy stocks. In 2026, careful monitoring of Chinese policy signals and economic data will be essential for understanding shifts in risk appetite and resource‑linked valuations.

Commodities and Energy: From Cyclical Trade to Strategic Assets

Commodity markets are at a crossroads in 2026. According to the World Bank’s Commodity Markets Outlook, global commodity prices are forecast to decline modestly but remain above pre‑pandemic levels, even as energy markets adjust to oversupply and demand shifts. Oil prices, for example, are projected to average lower in 2026 compared with recent years, reflecting ample supply and slower demand growth.

Uranium markets reflect this dynamic, with renewed interest in nuclear power as a stable low‑emissions energy source. Supply has been tight after years of underinvestment, making prices sensitive to shifts in policy and demand. Rare earth elements are also gaining attention because of their role in electric vehicles, renewable energy, and advanced manufacturing. Their concentrated supply chains have prompted nations to encourage diversified production.

In Australia, a major supplier of uranium, rare earths, and other critical minerals, this strategic demand supports commodity producers even amid broader price moderation. Investors should view energy and resource exposure through both a cyclical and structural lens, recognising the role these assets play in energy transition and industrial growth.

Policy Mistakes Are a Growing Risk

As central banks lower interest rates and governments consider fiscal support measures, the risk of policy errors increases. If rates are reduced too quickly, inflation could accelerate, forcing a reversal in monetary policy and tightening financial conditions. Trade barriers and protectionist measures could also contribute to cost pressures.

Investors should be aware that policy adjustments can create sharp shifts in market sentiment and valuations. Portfolios with heavy exposure to low‑rate scenarios or limited inflation protection may face headwinds if policies change direction. Incorporating real assets, inflation‑linked securities, and equities with pricing power can help manage these risks.

Geopolitics Is No Longer a Tail Risk

Geopolitical uncertainty has migrated from occasional headline risk to a persistent market variable that influences asset prices, supply chains and investor confidence. Tensions in commodity‑producing regions, evolving trade relationships, and political dynamics in major economies create a backdrop of fluid risk. In this setting, traditional diversification may not sufficiently buffer portfolios; instead, investors must assess how macro‑political developments translate into market exposures.

Investors should consider sector-level implications, including energy, defence, and semiconductors, as well as currency exposures. Scenario planning and real-time monitoring are critical for navigating rapid geopolitical shifts that may have asymmetric effects across industries and regions.

Balance Sheets and Cash Flow Matter More

In 2026, market performance is increasingly being driven by corporate fundamentals. Companies with strong balance sheets, stable cash flow and disciplined capital allocation are better positioned to withstand volatility and policy shifts. Firms reliant on cheap financing or aggressive expansion without profitable cores face greater valuation downside as markets become more discriminating.

This shift toward fundamental quality is apparent in both developed and emerging markets, where investors are applying tighter valuation lenses and rewarding companies that demonstrate sustainable earnings growth rather than thematic optimism. For portfolios, prioritising firms with financial strength and sustainable earnings can contribute to resilience throughout varied market conditions.

Returns Will Come From Selectivity, Not Broad Market Rallies

The cumulative effect of these themes is a market environment in which broad index exposure is less likely to capture differentiated returns. Instead, returns in 2026 are expected to come from selectivity—choosing exposure based on region, sector and company fundamentals rather than relying on broad market momentum. Valuation dispersion across regions and sectors is widening, creating opportunities for active managers and disciplined investors to capture outperformance.

Active stock selection that balances growth prospects with quality metrics, strategic exposure to structural themes such as strategic commodities and AI execution, and a diversified approach that incorporates inflation resilience and policy‑sensitive positioning can help portfolios navigate the complexity of 2026. For Australian investors, the interplay between domestic economic trends, commodities demand and global growth divergence will be a defining context for portfolio performance.

Navigating Complexity in 2026

Markets in 2026 will reward investors who combine strategic insight with disciplined execution. Companies with strong balance sheets, stable cash flows, and pricing power are likely to withstand potential policy missteps, inflation surprises, or market shocks. Exposure to structural growth areas such as AI, renewable energy infrastructure, and strategic commodities provides both upside and diversification. For Australian investors, this also means monitoring the domestic economy, including household consumption trends, commodity exports, and policy signals, to avoid overexposure to weaker local sectors.

Selective positioning will be essential. Portfolios that balance structural growth themes with defensive quality, including reliable dividend payers and companies with resilient earnings, can navigate volatility more effectively. Investors should also maintain flexibility across sectors and regions to capture pockets of opportunity created by the divergence in global growth. This approach allows portfolios to benefit from faster-growing markets in Asia, targeted growth sectors in the US, and resource-linked gains on the ASX.

Disciplined execution remains a cornerstone of success. Focusing on valuation, earnings quality, and long-term business sustainability helps ensure that thematic exposure translates into meaningful returns. Active monitoring of macroeconomic developments, AI adoption, and resource market trends enables investors to adjust positions in real time. By combining structural growth, defensive quality, and tactical agility, portfolios are better positioned to capture returns while managing the inherent complexity of 2026.

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

Big Tech earnings could shake your portfolio this week. Understand how the latest results may influence global markets, the ASX and your investment strategy.

A second strategic chokepoint is under threat after Hormuz. Discover how the Bab al-Mandeb blockade could affect oil prices, inflation, interest rates and your portfolio.

This week's Stock Spotlight is NYSE-listed JPMorgan Chase & Co. About JPMorgan Chase & Co. JPMorgan Chase & Co. operates as a bank and financial holding company in the United States, rest of North America, Europe, the Middle East, Africa, the Asia Pacific, Latin America, and the Caribbean. It operates in three segments: Consumer & Community Banking, Commercial & Investment Bank, and Asset & Wealth Management. The company offers deposit, investment and lending products, and cash management; mortgage origination and servicing activities; residential mortgages and home equity loans; and credit cards, payment solutions, travel services, merchant offers, lifestyle benefits, auto loans, and leases to consumers and small businesses through bank branches, ATMs, and digital and telephone banking. It also provides investment banking, market-making, financing, custody, and securities products and services; corporate strategy and structure advisory, equity and debt market capital-raising, and loan origination and syndication services; cash and derivative instruments, risk management solutions, prime brokerage, clearing, and research; and fund services, liquidity and trading services, and data solutions products for large corporations, financial institutions, merchants, start-ups, small and midsized companies, local governments, municipalities, nonprofits, and commercial real estate clients. In addition, the company offers multi-asset investment management solutions in equities, fixed income, alternatives, and money market funds to institutional clients and retail investors; retirement products and services, estate planning, lending, deposits, and investment management products to high-net-worth clients; and financial transaction processing. JPMorgan Chase & Co. was founded in 1799 and is headquartered in New York, New York. Source: EODHD Key Stats

This week's Stock Spotlight is NYSE-listed Wells Fargo & Company. About Wells Fargo & Company. Wells Fargo & Company, a financial services company, provides diversified banking, investment, mortgage, and consumer and commercial finance products and services in the United States and internationally. It operates through four segments: Consumer Banking and Lending; Commercial Banking; Corporate and Investment Banking; and Wealth and Investment Management. The company's financial products and services includes checking and savings accounts, and credit and debit cards, as well as home, auto, personal, and small business lending services. It also provides personalized wealth management, brokerage, financial planning, lending, private banking, trust and fiduciary products and services; and financial solutions to private, family owned and public companies through products and services including banking and credit products across multiple industry sectors and municipalities, secured lending and lease products, and treasury management. In addition, it offers a suite of capital markets, banking, and financial products and services, such as corporate banking, investment banking, treasury management, commercial real estate lending and servicing, equity, and fixed income solutions, as well as sales, trading, and research capabilities services to corporate, commercial real estate, government, and institutional clients. Wells Fargo & Company was founded in 1852 and is headquartered in San Francisco, California. Source: EODHD Key Stats

This week's Stock Spotlight is NYSE-listed Bank of America Corp. About Bank of America Corp. Bank of America Corporation, through its subsidiaries, provides various financial products and services for individual consumers, small and middle-market businesses, institutional investors, large corporations, and governments worldwide. It operates through four segments: Consumer Banking, Global Wealth & Investment Management (GWIM), Global Banking, and Global Markets. The Consumer Banking segment offers traditional and money market savings accounts, certificates of deposit and IRAs, checking accounts, and investment accounts and products; credit and debit cards; residential mortgages and home equity loans; and direct and indirect loans. The GWIM segment provides investment management, brokerage, banking, and trust and retirement products and services; wealth management solutions; and customized solutions, including specialty asset management services. The Global Banking segment offers lending products and services, including commercial loans, leases, commitment facilities, trade finance, and commercial real estate and asset-based lending; treasury solutions, and underwriting and advisory services. The Global Markets segment provides market-making, financing, securities clearing, settlement, and custody services; securities and derivative products; and risk management products using interest rate, equity, credit, currency and commodity derivatives, foreign exchange, fixed-income, and mortgage-related products. Bank of America Corporation was founded in 1784 and is based in Charlotte, North Carolina. Source: EODHD Key Stats

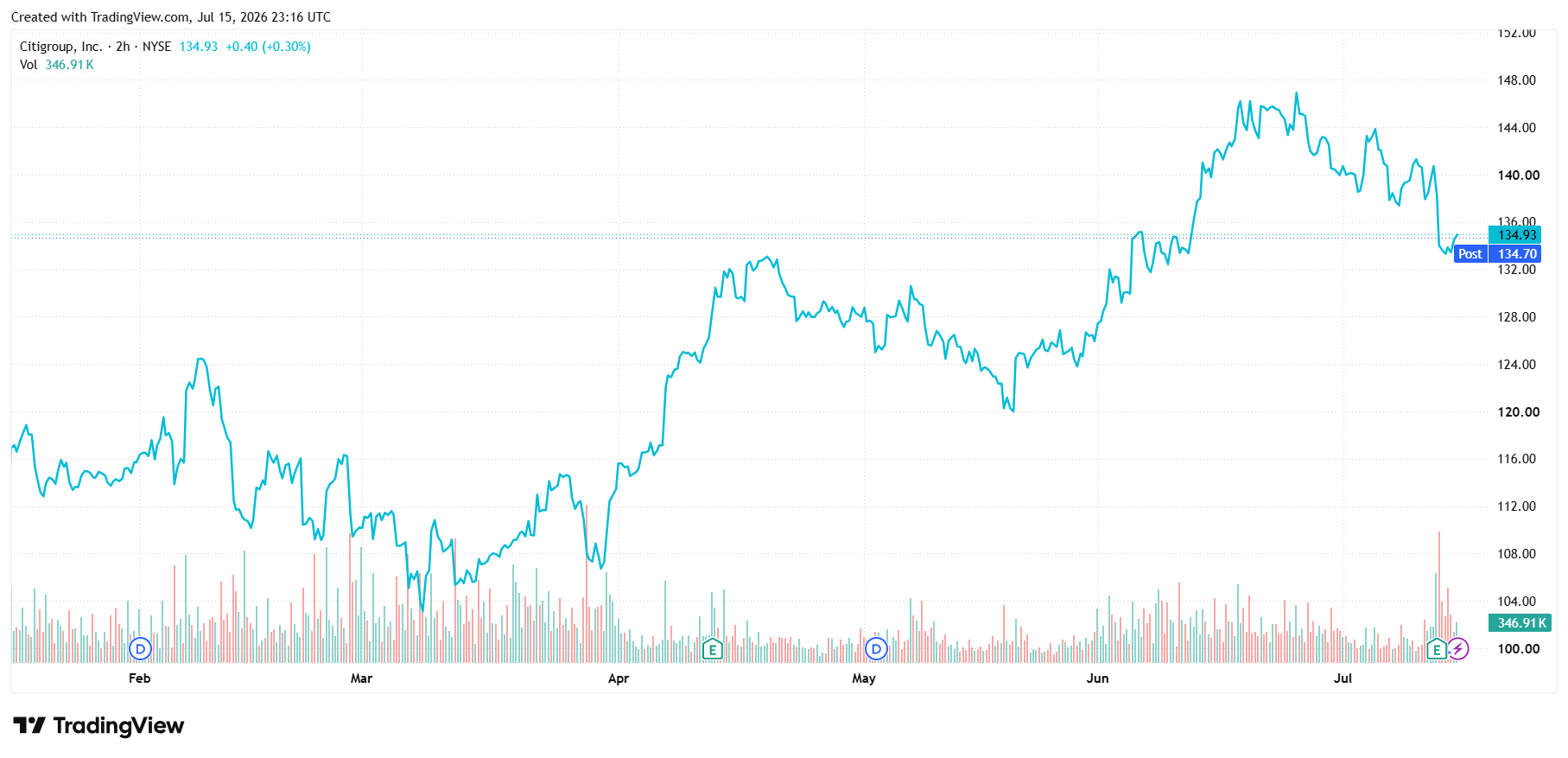

This week's Stock Spotlight is NYSE-listed Citigroup Inc. About Citigroup Inc. Citigroup Inc., a diversified financial service holding company, provides various financial products and services to consumers, corporations, governments, and institutions. It operates through five segments: Services, Markets, Banking, U.S. Personal Banking, and Wealth. The Services segment includes treasury and trade solutions, which provides cash management, trade, and working capital solutions to multinational corporations, financial institutions, and public sector organizations; and securities services, such as cross-border support for clients, local market expertise, post-trade technologies, data solutions, and various securities services solutions. The Markets segment offers sales and trading services for equities, foreign exchange, rates, spread products, and commodities to corporate, institutional, and public sector clients; and market-making services, including asset classes, risk management solutions, financing, and prime brokerage. The Banking segment includes investment banking services comprising equity and debt capital markets-related strategic financing solutions; advisory services related to mergers and acquisitions, divestitures, restructurings, and corporate defense activities; and corporate lending consists of corporate and commercial banking. The U.S. Personal Banking segment provides proprietary and co-branded card portfolios; and traditional banking services to retail and small business customers. The Wealth segment offers financial services to high-net-worth clients through banking, lending, mortgages, investment, custody, and trust product offerings; professional industries, including law firms, consulting groups, accounting, and asset management; and affluent and high net worth clients. The company operates in North America, the United Kingdom, Japan, North and South Asia, Australia, Europe, the Middle East, and Africa. Citigroup Inc. was founded in 1812 and is headquartered in New York, New York. Source: EODHD Key Stats

AI is driving unprecedented demand for data centres. Discover how the infrastructure powering AI is creating opportunities across energy, property and technology.

About Capstone Copper Corp. Capstone Copper Corp., a copper mining company, mines, explores for, and develops mineral properties in the United States, Chile, and Mexico. The company primarily explores copper, silver, gold, molybdenum, zinc, iron, cobalt, and other base metals. Capstone Copper Corp. is headquartered in Vancouver, Canada. Source: EODHD Key Stats

About Qualcomm Inc. QUALCOMM Incorporated engages in the development and commercialization of foundational technologies for the wireless industry worldwide. It operates through three segments: Qualcomm CDMA Technologies (QCT); Qualcomm Technology Licensing (QTL); and Qualcomm Strategic Initiatives (QSI). The QCT segment develops and supplies integrated circuits and system software with connectivity and computing technologies for use in mobile devices; automotive systems for connectivity, digital cockpit, and ADAS/AD; and IoT, including consumer electronic devices, industrial devices, and edge networking products. The QTL segment grants licenses or provides rights to use portions of its intellectual property portfolio, which include various patent rights useful in the manufacture and sale of wireless products comprising products implementing LTE, and/or OFDMA-based 5G products and derivatives; to use cellular standard-essential patents, including 3G, 4G and 5G for cellular devices. The QSI segment invests in early-stage companies in various industries, including 5G, artificial intelligence, automotive, consumer, enterprise, cloud, IoT, and extended reality, and investments, including non-marketable equity securities and, to a lesser extent, marketable equity securities, and convertible debt instruments. It also provides development, and other services and sells related products to the United States government agencies and their contractors. In addition, the company is also involved in Qualcomm government technologies and data center businesses. Further, it provides security and intelligence services for unmanaged networks through software-based network security solutions. QUALCOMM Incorporated was incorporated in 1985 and is headquartered in San Diego, California. Source: EODHD Key Stats

AI spending is accelerating in 2026. Learn how to read AI earnings, spot overhyped stocks and find companies converting AI investment into real profit.