Stock Spotlight: Computershare Ltd (ASX:CPU)

About Computershare

Computershare Limited provides issuer, employee share plans and voucher, communication and utilities, technology, and mortgage and property rental services. The company offers issuer services that include register maintenance, corporate actions, stakeholder relationship management, corporate governance, and related services; corporate trust comprises trust and agency services in connection with the administration of debt securities; mortgage services and property rental, including tenancy bond protection services; and employee share plans and voucher services comprising administration and related services for employee share and option plans, and childcare voucher administration services. It also provides communication services and utilities operations consisting of document composition and printing, intelligent mailing, inbound process automation, scanning, and electronic delivery; and technology services, such as software solutions in share registry and financial services, and operations and shared services functions, as well as the provision of transitional services. It operates in Australia, Hong Kong, Switzerland, New Zealand, rest of Asia, Canada, rest of Continental Europe, the United Kingdom, the Channel Islands, Ireland, Africa, and internationally. The company was incorporated in 1978 and is based in Abbotsford, Australia.

Key Stats

Key Stats

Source: Yahoo Finance. Data as of 05/08/25.

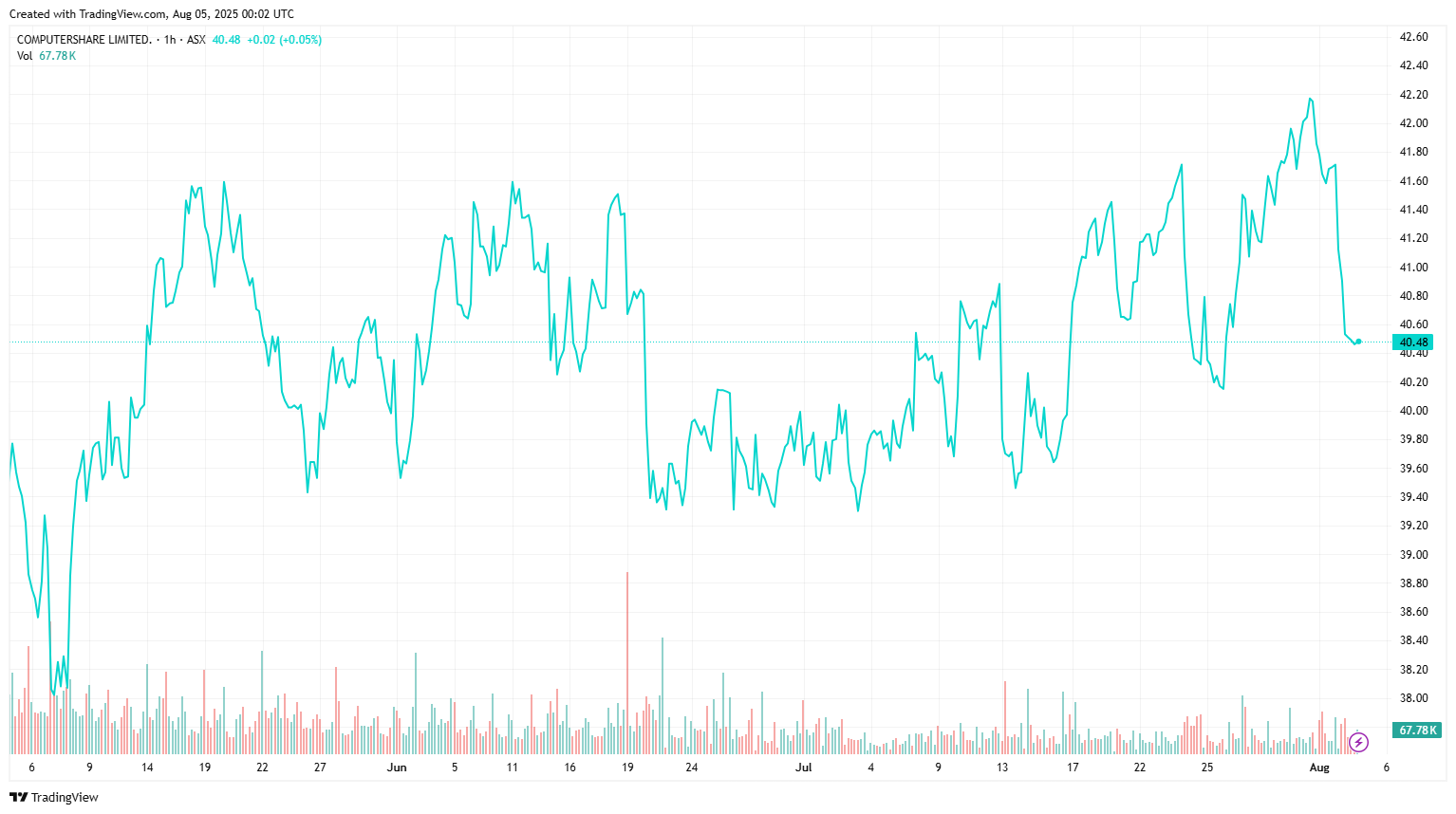

Price Performance

Growth Potential

- Provides some hedge against rising global interest rates.

- CPU is globally diversified with a revenue model that generates predictable recurring revenues and strong free cash flow generation.

- Two main organic growth engines in mortgage servicing and employee share plans should lead to organic EPS growth.

- Expectations of margin improvement via cost reductions program.

- Leveraged to rising interest rates on client balances, corporate action and equity market activity.

- Potential for earnings derived from non-share registry opportunities due to higher compliance and IT requirements.

- Solid free cash flow and deleveraging balance sheet.

Key Risks

- Increased competition from competitors such as recently listed Link and Equiniti which affect margins.

- Cost cuts are not delivered in accordance with market expectations.

- Sub-par performance in any of its segments, especially mortgage servicing (Business Services) as a result of higher regulatory and litigation risks; Register and Employee Share Plans as a result of subdued activity.

- Exchanges such as ASX are exploring blockchain solutions to upgrade its clearing and settlement system (CHESS). This distributed ledger technology can bring registry businesses in-house and disrupt CPU.

Subscribe to our newsletter

Disclaimer: This article does not constitute financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

Speak to an Advisor